Commentaires

From 2023’s surprises to 2024’s emerging opportunities

18 janvier 2024

Last week, the New York Times identified some pivotal themes set to shape 2024: elections, antitrust and shadow banking, painting a vivid tableau of the global investment landscape. Against this backdrop, over half the world’s population across more than 50 countries will choose their governments in 2024. The US is probably the most significant, but Taiwan’s on January 13 was also noteworthy in the context of the country’s tense relationship with China and its crucial role in the global technology sector and semiconductor manufacturing.

In antitrust, recent weeks have seen cancellations of deals such as Illumina and Adobe and losses in important cases for Google and Apple (with appeals underway). Many antitrust cases are expected to reach courts in both Europe and the US in 2024.

The shadow banking sector is also at the forefront, with prominent figures like Jamie Dimon of J.P. Morgan highlighting private credit as a potential harbinger of the next financial crisis.

Listen to Robert’s audio commentary:

Small caps in 2024

Turning to our universe of global small-cap equities, our outlook for 2024 builds on our December 2023 comment. As you may recall, 2023 was marked by the dominance of US large-cap equities, particularly the “Magnificent Seven” technology stocks. To help provide a well-informed outlook for this year, I reviewed our previous commentaries, all of which are available on our website from the time our firm was established. They offer valuable context and background and I invite you to browse them for a fuller picture of our thinking over time.

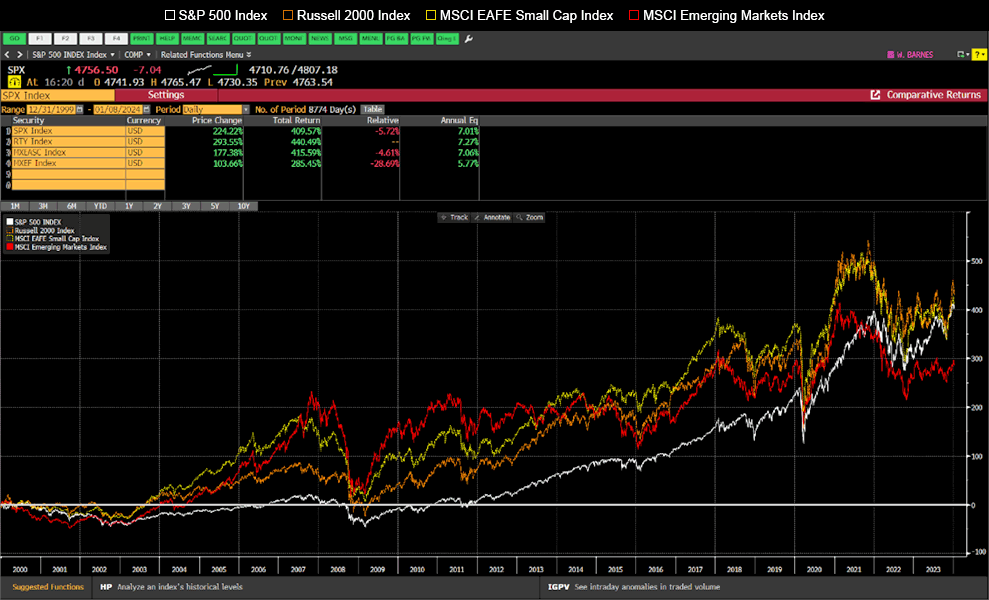

Despite the incredible returns of the Nasdaq-100 Index and, consequently, the S&P 500 Index due to unprecedented concentration, these large-cap indices have not significantly outperformed small caps since 2000, even in the face of various global upheavals, including the tech crash, the Great Financial Crisis and the COVID-19 pandemic.

Defying expectations: Large-cap vs. small-cap performance since 2000

Source: Bloomberg.

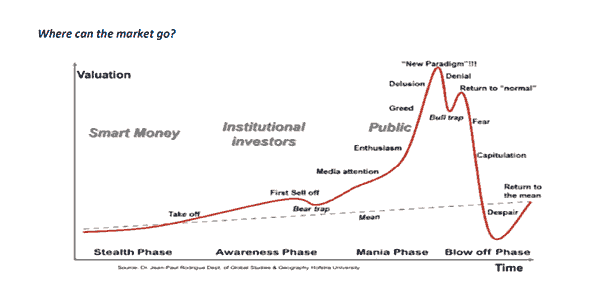

2024’s market moods

Understanding market psychology is a good starting point for thinking about the year ahead. So, where do we stand today?

We view the Nasdaq 100 and, by extension, the S&P 500 as being in the “New Paradigm” phase. Meanwhile, small-cap, international and emerging markets equities are approaching the “Despair” phase. Question is, when and what will trigger a return to the mean?

The concentration conundrum

The S&P 500 is at its highest concentration ever, with the top-10 stocks comprising 31%. This is in contrast to the 35-year average of 20% and even exceeds the 25% peak during the tech bubble. A look back at the performance of US large caps following the era of the Nifty Fifty, which dominated the markets in the 1960s, these stocks subsequently underperformed from 1973 to 1982, realigning their multiples with the broader market.

From 2000 to 2010, US large caps lagged most other indices by a wide margin.

Another perspective to consider is that the US’s weight in the MSCI World Index is at an all-time high of 70%, far exceeding its 25% contribution to global GDP. This is a stark increase from approximately 38% at the end of 2000.

According to the Buffett Indicator, which measures the total market cap over GDP, we are currently at 174%, another record high.

Now that we have scared you about the US large-cap market, the question remains: why do we anticipate a return to the mean in 2024?

Unprecedented global events: a four-year retrospective

The last four years have been extraordinary. In 2020, we had the COVID-19 pandemic, followed by a global lockdown, things we had never seen before. 2021 was the year of the reopening, although a few countries like China reopened in 2022. We also saw the rise of inflation. Not so transitory as it turned out, although the supply chain shocks were. 2022 was the year of the great interest rate resets around the world and the end of free money. Rates were no longer zero. We also saw the war between Russia and Ukraine break out last February. 2023 could have been a more normal year, maybe marked by a slowdown or recession caused by the rapid rise in interest rates. Instead, the economy continued to be strong.

The overlooked factors of government spending and consumer behaviour

What did we miss? First, we missed the fact that governments around the world continued to spend enormously, while running huge deficits. The US, for example, ran a deficit for fiscal 2023 (October) of $1.7 trillion, $320 billion (23%) more than in 2022 and 6.3% of its GDP.

Second, we did not think Americans would spend all the excess savings they had built up during COVID-19.

Source of excess savings

Source: Federal Reserve.

Third, we did not anticipate the frenzy brought by the launch of ChatGPT and the narrative around generative AI.

Fourth, we did not anticipate such an aggressive Fed pivot while inflation is still running hot. Is the Fed seeing a market slowdown ahead?

Navigating new normals

So, what do we think is in store for 2024?

- The pandemic is over. Although COVID-19 persists, it is no longer seen as a flu variant. No more lockdowns. And companies in 2024 will stop the references to 2019.

- Interest rates have more or less reached a peak. Will they come down fast? We do not think so unless we experience a deep recession and even then, they will not go back to 0. That experiment failed and the central banks admit it. Will they go from 5% to 10% as they did from 0 to 5%? We believe absolutely not.

- Supply chain shocks have subsided. There are always supply chain snags, but what we saw in 2021 and 2022 is now behind us.

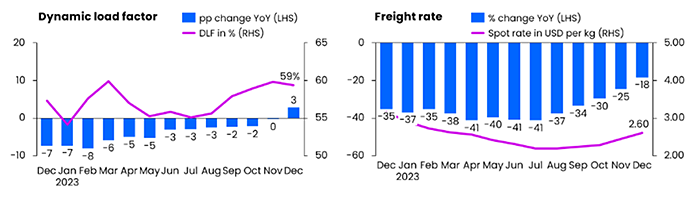

- The easy comparison for inflation is now over. Comparing 2023 prices to 2022 showed a big decline. Comparing 2024 to 2023 will not be so straightforward. We will realize that inflation is stickier. How central banks will react remains to be seen. See air freight rates as an example:

Source: Xeneta.

- The return of the bond vigilante: Those government deficits are unsustainable and the amount of government debt to be refinanced in 2024 is staggering. Governments will have to go back to austerity, possibly at the worst possible time if the economy slows down. We will also see income taxes rise, particularly for companies with high profitability and aggressive tax strategies.

- The lagging impact of interest rate increases: It takes about 18 months to see the full impact of interest increases. So, we will see the impact of increases for another year, even if rates come down quickly.

- A return to investment fundamentals: 2023 was brutal for many fundamental investors, us included. Dividend-paying companies underperformed non-dividend payers by the largest margin since 1983. Companies with strong balance sheets underperformed the weakest. Companies with low valuations underperformed those with high valuations.

- Emphasis on revenue and EPS growth: In 2023, steady revenue and earnings growth gave way to momentum and liquidity. A good example is Apple, which saw its share price increase 49% in 2023 despite a 3% revenue decline in FY 2023 (September) and no earnings growth. That share price increase was equivalent to close to a trillion dollars, the market cap of Australia’s, South Korea’s or Stockholm’s stock exchanges. We anticipate a different trend this year, with a focus on solid balance sheets to withstand shocks and higher interest rates and to take advantage of consolidation opportunities.

- There will be more M&A, both from strategic investors as well as private equity funds. A more stable operational and funding environment will be conducive to transactions.

- We may also see a return of individual investors in Japan now that the Nikkei Index is back to where it was in 1990 and the government is trying to unlock US$14 trillion of household savings by expanding the tax-exempt Nippon Individual Savings Account (NISA), allowing investors to buy up to $24,170 per year in stocks. Japanese households keep 54% of their assets in cash versus 35% in the euro area and 13% in the US.

Building trust through market cycles

For our clients who started investing with us between 2019 and March 2020, you will have experienced mediocre performance, even worse if you invested with us in spring 2020 or since March 2022. But likely satisfactory if you invested with us outside these periods.

Should you keep your trust in us? We believe you should.

Our portfolio management team remains the same. The five partners who manage our one portfolio as one team have been together for over 15 years.

We have added to our bench strength with five more analysts joining our developed market portfolio management team since 2018 and three more covering emerging markets.

Upholding our investment philosophy

Our philosophy remains the same. We believe:

- Earnings growth drives stock prices.

- Secular trends will support superior and longer-term growth.

- A long-term investment horizon is key.

Our investment process is solid:

- Add excellent investment ideas that meet all our criteria, including valuation and expected return, to an approved list.

- Use the approve list to build a portfolio that meets client expectations and constraints.

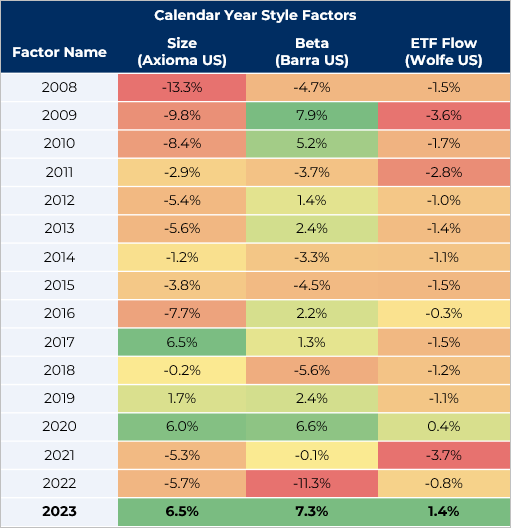

The chart below shows some style factors since 2008. Our worst two years since inception have been 2020 and 2023. Unfortunately, this has impacted our one to four-year performance. As illustrated, those two years coincided with size (larger), beta (higher) and ETFs (passive flows) outperforming.

You will also notice that the number of years these factors underperformed greatly surpass the number of times they outperformed, forming another reason for our optimism.

Calendar year style factor returns

Source: Omega Point.

As we reflect on these trends and look ahead, it’s clear that the markets are in flux. We remain committed to adapting to these changes, always with an eye on long-term growth.

With this perspective, I want to wish you an excellent 2024. May the year bring health, peace and happiness to you, your families and your friends and colleagues!

Robert Beauregard

President, Co-Founder and Chief Investment Officer

*This communication may contain forward-looking statements (within the meaning of applicable securities laws) relating to the business of our funds and the overall financial environment in which they operate. Forward-looking statements are identified by words such as “believe”, “in our opinion”, “anticipate”, “project”, “expect”, “predict”, “intend”, “plan”, “will”, “may”, “estimate” and other similar expressions. These statements are based on our expectations, estimates, forecasts and projections and include, without limitation, statements regarding decreased fund portfolio risk and future investment opportunities. The forward-looking statements in this communication are based on certain assumptions; they are not guarantees of future performance and involve risks and uncertainties that are difficult to control or predict. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements. There can be no assurance that forward-looking statements will prove to be accurate as actual outcomes and results may differ materially from those expressed in these forward-looking statements. Readers, therefore, should not place undue reliance on any such forward-looking statements. Further, these forward-looking statements are made as of the date of this communication and, except as expressly required by applicable law, we assume no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.