Commentary

Our views on small caps

December 21, 2023

Recent market movements have been driven by a decline in bond yields and a repricing of a more optimistic scenario, where growth is resilient and inflation figures are falling fast. While mid-term trends look supportive, persistently high inflation could point to later interest rate cuts than markets currently expect.

Small caps shine in Europe

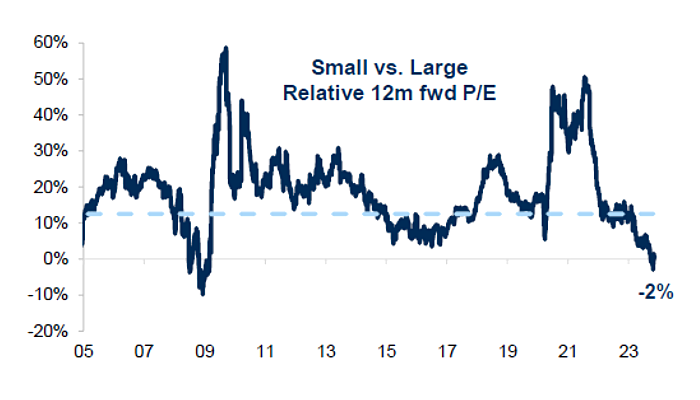

We believe that growth will remain steady in 2024 despite potential economic contractions in some regions during the first half of the year. European small caps continue to look attractive compared to their larger counterparts. As illustrated below, small caps are near their largest historical discount relative to large caps. Several industries still trade at very low valuations and could benefit from a potential re-rating. We believe the end of the destocking phase combined with lower interest rates should help in regaining momentum for European small caps.

P/E of STOXX small caps vs STOXX large caps

Source: Goldman Sachs.

Wage growth: a silver lining

Real wage growth is another indicator showing positive signs. An increase in wage growth could be beneficial for consumers and the broader economy. Companies’ responses to growing labour costs will be a key determinant for financial markets in 2024. Companies with strong pricing power should be able to raise prices again. Others might scale back labour, cut investments or accept lower profits. In summary, we expect earnings growth to be erratic and modest in 2024.

Factor investing in a dry liquidity climate

Regarding factor investing, liquidity has dried up in 2023 and small caps are underinvested in compared with other asset classes. According to JP Morgan, small caps in Europe have experienced their worst 23-month outflows in the last 15 years. However, November’s positive inflows may indicate a shift toward a more optimistic sentiment. A return to more normalized monetary policy should gradually improve liquidity and investment flows during 2024. Much like the adage “cash is king,” investors are likely to continue rewarding companies with decent dividends and buybacks.

M&A: the untapped potential for small caps

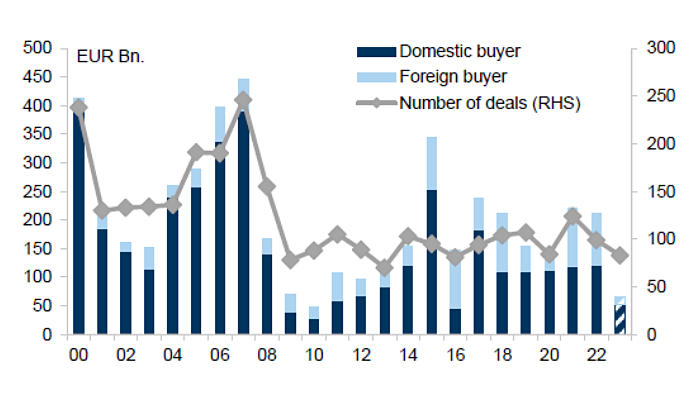

M&A activity is another potential catalyst that would favour smaller companies. M&A in 2023 has been low, as shown by the chart below, with a 70% decrease primarily due to fewer foreign buyers. Corporate sentiment, equity valuations and monetary conditions are key drivers of M&A activity. Reasonable equity valuations along with a normalizing monetary policy should enhance corporate sentiment toward M&A. With positive sentiment and plenty of balance sheet resources, a potential pickup in M&A could greatly benefit smaller companies.

Sources: Goldman Sachs, Bloomberg.

Navigating tomorrow’s market

As small caps gain traction and M&A activity hints at resurgence, the market presents a complex puzzle. The real insight emerges in piecing together these fragments to understand where the next wave of growth will come from.