Commentary

Made in China Mexico

November 23, 2023

Within the emerging market universe, plenty of ink has been spilt on extreme pessimism regarding China and over-the-top optimism around India. Yet, as the following chart shows, small-cap stocks in Mexico have quietly been a top performer in the post-pandemic period.

Mexico’s unforeseen rise

Growing tension between China and the US has positioned Mexico as an unintended beneficiary due to its geography and the trend among companies to shock-proof their supply chains through nearshoring.

Will this time be different?

As noted in an earlier weekly, we recently met with companies across various sectors in Mexico and most of the executives we spoke to seemed convinced that the nearshoring wave was sustainable while also being realistic about the challenges ahead.

They have good reason to be pragmatic. The last time the economic stars aligned for Mexico via NAFTA (North American Free Trade Agreement) in 1994, the country delivered mediocre growth of around 2% and watched on the sidelines as China took full advantage of a shift in manufacturing from the West. The question now is if the outcome will be any different this time.

The nearshoring challenge trifecta

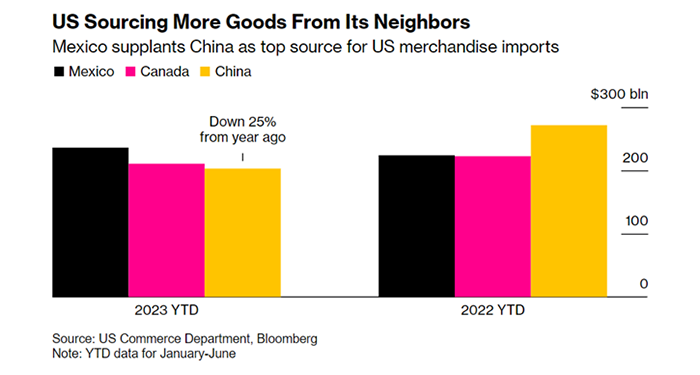

Mexico’s ascent as a key supplier to the US can be traced to three key events: Trump’s tariffs on China in 2018, the US-Mexico-Canada Agreement (USMCA) that raised the bar for North American product content requirements and pandemic-induced supply chain disruptions. These factors, coupled with deteriorating US-China relations, have led to Mexico surpassing China as a supplier to the US this year.

However, as emerging market investors, we know that structural tailwinds that are attractive and advantageous today don’t preordain good outcomes. Our conversations with Mexican executives at the recent LatAm conference gave us a good reality check on the constraints they face on the ground, from infrastructure and water supply to the political climate.

Electric dreams, grounded realities

While Mexico generates sufficient power, it struggles with inadequate transmission infrastructure in its north that hinders industrial growth. We spoke to two industrial REIT developers that had to build their own power systems, passing those costs to customers. For perspective, Mexico’s state utility, CFE, built 150 kms of transmission lines in 2022 compared to Brazil’s Electrobras’ 8,679 kms.

Parched prospects

Water availability is another constraint, especially in Nuevo Leon, home to the populous city of Monterrey and the large, water-hungry beverage industry that includes Heineken and Arca Continental, one of Latam’s largest Coke bottlers that extracts billions of gallons of water under federal concessions. As recently as 2022, Mexico had declared a drought in the state of Nuevo Leon and yet Tesla plans to open a factory there.

The political maze

The final speed breaker to the nearshoring story could be politics and a volatile security situation by the US border. On the political front, Mexico’s President recently demanded that airport operators in Mexico reduce their tariffs even though they were bound by law via a concession system instituted in 1998. In terms of security concerns, the cities of Juarez and Tijuana, while strategically located across the border from California and Texas, have a history of gang violence and cartels profiting from piracy and counterfeiting.

Mexico’s unique competitive edge

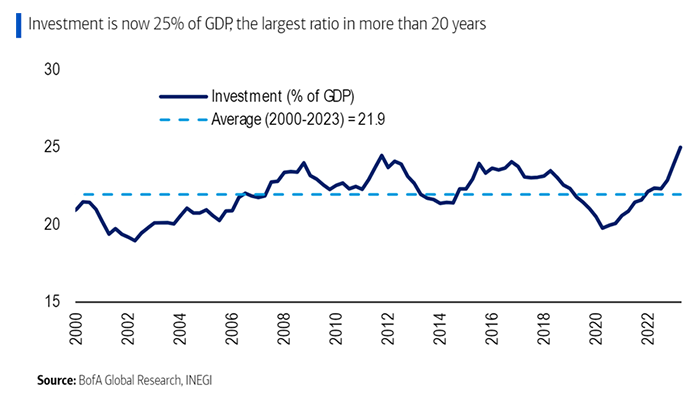

Despite these hurdles, Mexico offers several advantages, including lower labour costs compared to China, a younger workforce and significant investment in GDP, particularly in nearshoring and public infrastructure projects.

Unlocking nearshoring potential

With plenty of natural resources, a faster lead time and shorter distance to market, we think Mexico can continue to benefit from current trends with some policy support. Our Mexican holdings offer three different ways to access the nearshoring theme.

Grupo Cementos de Chihuahua (GCC MM) – Primarily selling cement in the US, GCC also operates in Chihuahua. It benefits from strong volume demand generated by the region’s growing industrial sector, particularly maquiladoras and warehouses near the Texas border. Recently, GCC expanded its Samalayuca plant and now supplies cement to about 85 projects in Northern Mexico, serving clients like Foxconn, Wistron and Pegatron.

Regional SAB de CV (RA MM) – Known as “Banregio,” this Mexican bank specializes in lending to small and medium enterprises, with a strong focus in Neuvo Leon, its home state and a big beneficiary of the nearshoring trend. With about 45% of its assets in the region, Banregio is poised to benefit from the growth of industries supporting multinational corporations relocating to Mexico, thanks to low credit penetration and an expected easing cycle.

Grupo Aeroportuario Del Centro Norte (OMAB MM) – OMA, managing 13 airports in Central and Northern Mexico, sees its largest traffic accounting for nearly half of its total at Monterrey Airport. Despite recent concerns about tariff cuts, we remain positive on OMA both for its exposure to nearshoring and potential for growth in its commercial business. The company operates six airports closely tied to nearshoring, covering 33.5 million square metres of industrial gross leasable area, about 35% of Mexico’s total.

A crucial crossroads

The real intrigue lies not in what Mexico has already achieved, but in what it could accomplish moving forward. Will it leverage its current position to create a more diversified, resilient economy, or will it repeat the patterns of the past? As global dynamics continue to shift, Mexico could be a big winner and serve as a blueprint for other emerging markets navigating the balance between risk and opportunity.