Commentaires

What’s the deal with EM small cap

19 janvier 2023

For fans of Seinfeld, the line “What’s the deal with…” reminds us of a particular brand of observational comedy from the 90’s. Well, turns out 90’s humor is still a big deal, as Netflix paid half a billion dollars in 2021 for the streaming rights of Seinfeld. Not bad for a show about nothing. As we kick off a brand-new year, we thought it’s the perfect time to ask ourselves “What’s the deal with EM small cap…?”

For most investors, emerging markets (EM) as an asset class is high on the risk spectrum. They could be forgiven for thinking of small caps within EM to be a step too far. The EM small cap universe (EM SC) for the most part is ignored or misunderstood. We hope to change a few perceptions along the way by shining a light on EM SC as potential ground for adding alpha.

Added value

Before we begin to answer “What’s the deal with EM small caps…” let’s look at how MSCI EM SC has performed compared to its all-cap counterpart, MSCI EM. As seen below, whether on a three year, five year, 10 year or 20 year period, the MSCI EM SC index adds value compared to its all-cap counterpart. At the start of 2023, as we possibly enter a prolonged period of higher inflation and interest rates, we expect small caps to outperform by leveraging the flexibility and nimbleness that comes with smaller size and lower bureaucracy.

% Annualized USD Returns

| 3 yr | 5 yr | 10 yr | 20 yr | |

|---|---|---|---|---|

| MSCI EM SC | 5.38% | 1.32% | 3.45% | 9.60% |

| MSCI EM | -2.42% | -1.10% | 1.77% | 9.04% |

A big stage

The reasons for its relative outperformance are many. Let’s start off with the fact that the EM SC universe is vast, with plenty of space to find the next big compounder among 11,000 companies, 24 countries and 11 sectors. The benchmark index – MSCI EM SC (MXEFSC) – is constructed with no index weight bias. Also, except for Taiwan, there is no sector bias among the big countries that constitute the index. This size and diversity mean that the EM SC universe offers plenty of scope for portfolio diversification and alpha generation.

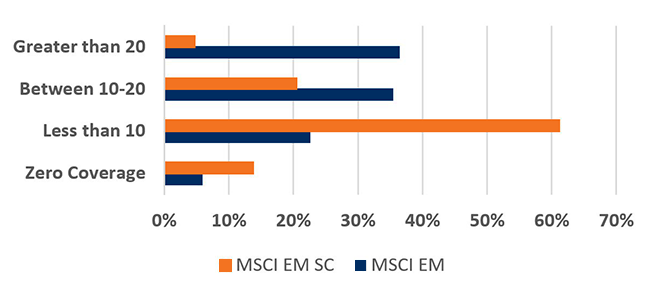

Low to no coverage

With big size comes lack of proper coverage. This universe’s vastness, combined with liquidity constraints, means this asset class doesn’t get extensive coverage, despite the value it has added historically. We see under coverage from both the buy side and sell side. This lends perfectly to our process at Global Alpha where we put in the hard yards to travel, meet management in person, and understand local business customs to stay on top of the story.

Analyst Coverage Comparison

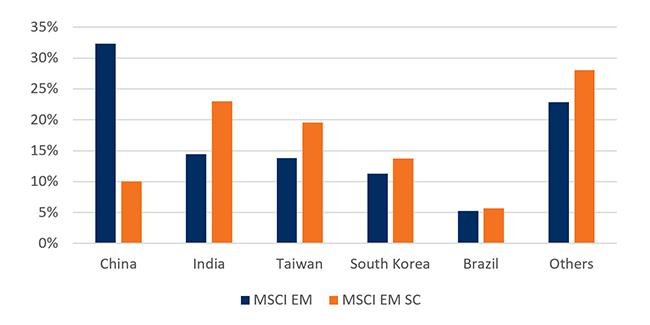

Less sino-centric

China dominates the large cap index – making up over 30% of the benchmark – while making up just around 10% of the small cap index,as seen in the graph below. The more balanced construction of the EM SC index helps investors avoid the policy and geopolitical risk that comes with concentrated exposure to a single market. At the same time, this differentiated exposure is a good complement in terms of total portfolio diversification.

EM Index Composition

Tailwinds

After decades of globalization, the pandemic exposed the fragility of the global supply chain system. De- globalization, near shoring and a greater reliance on domestic consumption as an engine of growth could come to define the next decade. EM small caps have greater exposure to consumer-facing sectors like healthcare, industrials, and discretionary and lesser exposure to global cyclicals like IT and energy compared to its all-cap peer.

MSCI EM

Source – Bloomberg. As on 30 Dec 2022

MSCI EM SC

Source – Bloomberg. As on 30 Dec 2022

SOE’s are minor actors

The EM SC benchmark has a lower allocation to State-Owned Enterprises (SOEs) than its large cap counterpart. Our experience informs us that SOEs are the same regardless of the country in which they are domiciled. They suffer from:

- poor capital allocation,

- lack of alignment of incentives,

- slow pace of decision making, and

- a track record of poor shareholder returns.

On the flip side, many of our small cap names need to be nimble and innovative to survive. Experience has shown that first generation entrepreneurs with skin in the game and properly aligned incentives tend to create shareholder value in the long run.

Being active

Emerging markets is a space where portfolios can look different from benchmarks. Research confirms that the average active share in this space has historically been close to 70%* and that there is a positive and significant relationship between active share and fund performance. Further, being consistently active is a strong predictor of fund performance. In other words, managers who back themselves on their ability to outperform by maintaining a high level of active share do well in the long run.

As we travel around the world, we are also seeing a generational shift in thinking among many of our family-owned companies. There is an openness among them to hire professional management. We also see a willingness to enhance corporate governance standards, and a better appreciation of what constitutes good capital allocation. While we don’t underestimate the challenge of finding the next HDFC Bank or TSMC, we feel the EM SC space offers the best playing field to generate value for our clients in the long run. And in our mind, that’s a big deal.

*Based on 67 emerging market funds that use MSCI Emerging Market Index as their benchmark. Active share is defined as percentage of holdings in a portfolio that differs from its benchmark.