Commentaires

The land of silk and money

14 mars 2024

One of the perks of being on the road to meet our holdings is the opportunity to see firsthand the daily challenges of running a business. It’s often said that the devil is in the details, and this holds particularly true in emerging markets, where every few kilometres bring a change in culture, customs and language. Some industries demand more from their execution strategies than others, with the microfinance sector standing out due to its complexity. While simple in concept, providing loans to underserved populations is more nuanced in practice.

The birth of microfinance

The microfinance business has its origins in Bangladesh, where Nobel Laureate Mohammed Yunus discovered that, despite their lack of resources, the impoverished were neither lacking in financial savvy nor in reliability as borrowers. In 1983, Yunus founded Grameen Bank, focusing on the strengths of his clients, including trustworthiness and creativity, rather than their lack of formal education or financial resources.

One of our holdings, CreditAccess Grameen (CREDAG IN), mirrors Grameen Bank’s business model and name. Our recent visit with CREDAG allowed us to observe its operations and engage with its customers, 99% of whom are women. As India’s largest microfinance institution, with 1,900 branches, 4.6 million clients and $2.7 billion in assets under management, CREDAG in our view exemplifies how to handle the complexities of a demanding businesses.

Ground-level insights

CREDAG’s strategy emphasizes local engagement and consistently doing the “little things” right. In a nation with 22 official languages, having branches staffed by locals who understand the regional dialect and economy are key. This local presence marks many employees’ first foray into the formal job market, fostering a strong sense of loyalty among them.

Outside a typical rural CREDAG branch in rural Bangladore.

We got to see CREDAG in action, where morning efforts focus on collections and afternoons on new client acquisition. The company’s investment in employee wellbeing, evidenced by providing kitchen spaces, covering grocery costs and reimbursing fuel expenses, further translates to high employee loyalty.

Relationship building – more than just transactions

The local economy in the villages we toured is driven by dairy and silk farming. In fact, the district is India’s largest cocoon silk producer.

A CREDAG client with her home silkworm business. The silkworms are feeding on mulberry leaves.

Silkworm cocoons in a bamboo tray for the local wholesale market.

Building customer relationships

Our participation in collection meetings highlighted the importance of CREDAG’s joint lending model.

A CREDAG collection meeting outside the village temple.

Meetings start and end with pledges, underscoring the powerful psychology of positive reinforcement to change borrowers’ behaviour for the better.

Leadership within borrower groups streamlines the payment process, allowing for relationship building, educational and sales opportunities. With most of its customers having no credit history or verifiable income, local connections (and intelligence) become crucial parts of good underwriting.

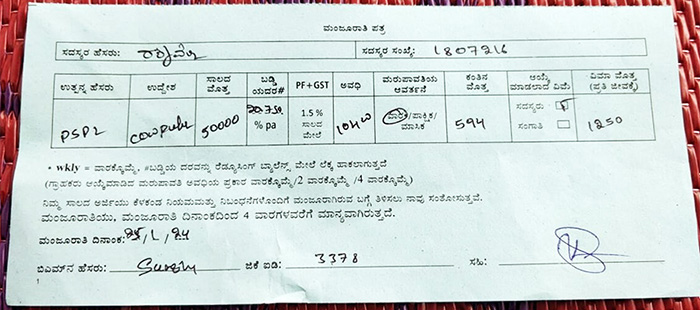

We also had the chance to see an income-generation loan being paid out to a dairy farmer.

Receipt for a 2-year, Rs 50,000 loan for buying a cow to be repaid in 104 installments.

Customized innovation: tradition meets tech

CREDAG leads in integrating technology, reducing client onboarding times and introducing new products rapidly. Its core banking solution caters to remote areas. Even with no internet connection, loan applications can be processed offline and then bulk uploaded when access is available. This allows CREDAG to offer flexible repayment options that align with its customers’ income cycle and new products like gold loans to reduce product time to market.

We also saw its technology in action. CREDAG offers cash emergency loans of up to RS 1000 as a complimentary service to creditworthy customers. This is especially beneficial to those in far-flung areas with no nearby bank branch. Customers can scan their biometric details to pull up their account information on the loan officer’s tablet. Once account details are verified, cash is disbursed on the spot. The whole exercise takes less than five minutes!

A CREDAG customer getting her biometrics scanned for account verification.

Details, details, details

Our visit with CREDAG reinforced how small details matter in building loyalty and maintaining operational efficiency. In the case of CREDAG, it translates to a best-in-class cost structure and customer retention ratio. While we recognize the inherent cyclicality of the microfinance sector, our visit helped us appreciate the need for rigorous execution and a deep understanding of the local context to achieve operational excellence.