Commentaires

Rethinking Indonesia: From near-term pain to long-term gains

27 mars 2025

In early March, our emerging markets team traveled to Jakarta, Indonesia. Given the political transition following the presidential election last year and ongoing macroeconomic headwinds, we sought to assess the market firsthand. For bottom-up investors, Indonesia has long been one of the most promising equity markets in Emerging Asia, and despite near-term challenges, we continue to see compelling long-term investment opportunities.

Jakarta can be a difficult city to navigate, but with the onset of Ramadan, the usual congestion was noticeably lighter, allowing us to efficiently move between meetings. As the world’s largest Muslim-majority country, Indonesia experiences notable shifts in consumer behavior and urban activity during the holy month. While moving around the city, we were particularly impressed by the quality of Jakarta’s road infrastructure, which, in many areas, exceeds what we have seen in the capitals of more developed countries. The improvements in connectivity and urban planning are a testament to Indonesia’s infrastructure investments over the past decade. Over the course of the week, we met with companies across the consumer, healthcare, real estate and industrial sectors, gaining valuable insights into the country’s evolving economic landscape.

A recurring theme in our discussions was the growing fragility of the Indonesian consumer, particularly in Java, the most economically and demographically significant of Indonesia’s 17,000 islands, accounting for 56% of the population and 57% of GDP. Over the past few years, real wage growth has lagged inflation, eroding purchasing power across all income segments. However, while businesses serving the urban middle class are experiencing a notable slowdown, some ex-Java regions have shown resilience, benefiting from recent minimum wage increases, social aid for low-income groups, commodity-linked employment and past infrastructure investments.

This consumer sentiment is most evident in downtrading, as households opt for cheaper alternatives across food, personal care and general merchandise. A notable trend has been the shift away from multinational companies, such as Unilever, in favour of more affordable local alternatives that offer comparable quality at lower price points. Companies in healthcare and discretionary retail are reporting lower volumes, even as premium segments remain more stable. Our meetings and channel checks confirmed that consumption weakness among middle-income consumers is entrenched, creating a challenging near-term outlook for businesses exposed to domestic demand.

The continued depreciation of the rupiah adds to the pressure. The currency is among the worst-performing in Asia year to date, despite active central bank interventions. Foreign investors have pulled USD1.8 billion from Indonesian equities this year, and on March 18, the Jakarta Composite Index triggered a trading halt after a 5% intraday drop, highlighting nervousness in the local market.

Although the new government has set ambitious economic targets, many investors remain cautious about execution risks. President Prabowo has announced a goal of achieving 8% GDP growth, a level Indonesia has not seen since 1995. With structural constraints and weak private sector investment, breaking out of the 5% growth range recorded in recent years remains a significant challenge.

One of the government’s most ambitious initiatives is the Danantara Sovereign Wealth Fund, designed to consolidate state-owned assets and fund strategic projects. Danantara has a goal of reaching USD900 billion in assets under management, which would make it one of the largest sovereign wealth funds globally. However, questions remain about its governance, transparency and the potential impact on state-owned enterprises (SOEs). With Danantara expected to rely on SOE dividend payouts, banking and energy sectors could see their capital allocation priorities altered.

At the same time, the government’s pivot away from infrastructure spending raises concerns about long-term economic sustainability. Over the last decade, Indonesia’s growth has been supported by significant public infrastructure projects, such as the Trans-Java Toll Road, which improved connectivity and regional economic development. The decision to reallocate resources toward populist policies, such as the free school meal program, has introduced fiscal uncertainties, particularly as recent revenue collection fell short of expectations.

Implementing free school meal programs has proven effective in combating malnutrition and improving educational outcomes in various countries. For instance, India’s Mid Day Meal Scheme, which serves nutritious lunches to over 97 million children daily, has led to increased school attendance and a 31% reduction in anemia prevalence among adolescent girls. However, executing such an initiative across Indonesia’s vast archipelago presents significant logistical challenges. Ensuring the consistent distribution of fresh meals to remote and diverse regions requires substantial infrastructure and coordination efforts.

Beyond economic policies, we noted concerns about the rising military presence in government institutions, a development that some investors worry could signal a shift toward a more centralized power structure. While Indonesia has undergone remarkable democratic progress since the fall of Suharto’s authoritarian rule in 1998, memories of military-dominated governance still linger. While this shift has raised alarms among some observers, it is important to distinguish today’s political landscape from the Suharto era, as institutional limits on military influence have since been established.

For foreign investors, rule of law, policy predictability and strong institutions remain critical factors in assessing investment opportunities. Any perception of reduced transparency or shifts away from a market-driven economy could weigh on investor sentiment. While the trend warrants monitoring, fears of a full-scale return to military-dominated governance appear overstated.

Despite macro headwinds, Indonesia continues to offer structural advantages that make it one of the most attractive long-term investment destinations in Emerging Asia. With a population of over 270 million and a median age of just 30, the country remains one of the largest and youngest consumer markets globally.

Amid the macroeconomic pressures, healthcare remains one of Indonesia’s most resilient sectors, driven by rising demand and structural under-penetration. The country’s healthcare expenditure stands at only ~3% of GDP, one of the lowest in ASEAN, with the doctor and hospital bed ratios per 1,000 inhabitants (0.7 and 1.2, respectively) remaining well below the global average. The positive demographic trend and government-backed healthcare program (BPJS Kesehatan) continue to support patient volumes, with private hospital networks benefiting from both scale efficiencies and growing intensities. As Indonesia works to improve access to quality healthcare and expand private insurance adoption, the sector presents compelling long-term growth potential, even in a more challenging economic environment.

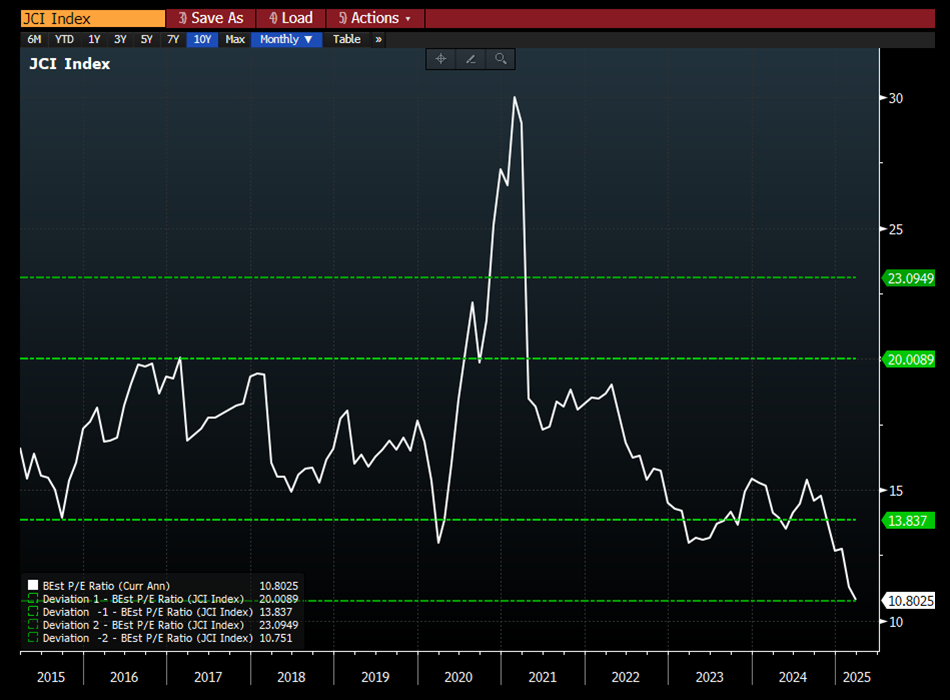

Indonesia has demonstrated resilience through past economic cycles, maintaining a relatively strong external position with foreign exchange reserves of approximately USD155 billion and government debt at ~39% of GDP. In 2024, the country recorded a current account deficit of 0.6% of GDP and a fiscal deficit of 2.3% of GDP, both within a manageable range for an emerging market. From a valuation perspective, Indonesian equities are now trading at very compelling levels, with the Jakarta Composite Index (JCI) at ~11x forward P/E, roughly two standard deviations below its 10-year average.

Source: Bloomberg

If global monetary conditions ease, Indonesia could be well-positioned for a rerating.

In this environment, stock picking is key. We continue to focus on companies with strong pricing power, resilient demand drivers and long-term structural advantages – qualities exemplified by our holdings in Sido Muncul and Mitra Adiperkasa.

Industri Jamu Dan Farmasi Sido Muncul Tbk PT (SIDO IJ) is Indonesia’s leading producer of traditional herbal medicines and functional beverages. Its flagship brand, Tolak Angin, is synonymous with natural flu and cold relief, commanding a market share of 72% in the herbal cold symptoms product category and enjoying strong consumer loyalty and premium pricing power while remaining a staple of Indonesian households. The company’s vertically integrated supply chain improves cost efficiency, further strengthening its margin resilience in an inflationary environment. Unlike many consumer goods companies that face pressure from rupiah depreciation, Sido Muncul is largely insulated from currency volatility as its raw material sourcing and key input costs are primarily local. With a net cash position and ~7% dividend yield, Sido Muncul combines defensive qualities with long-term structural growth, supported by expansion into functional beverages and overseas markets.

Mitra Adiperkasa Tbk PT (MAPI IJ) is Indonesia’s largest specialty retailer, operating a diverse portfolio of global brands, including Zara, Sephora, Nike, Starbucks and Apple (via authorized retail partnerships). The company benefits from strong pricing power through exclusive brand partnerships and a premium positioning, which allows it to maintain healthy performance even in softer consumption periods. While mass-market retail faces headwinds, Mitra Adiperkasa is well-positioned in the more resilient mid-to-premium consumer segment. Its long-term structural advantages stem from strong brand relationships, a well-executed omnichannel strategy and a track record of navigating economic cycles, making it a long-term winner in Indonesia’s evolving retail landscape.

Indonesia is experiencing a challenging economic transition, but its long-term structural advantages remain intact. Our Indonesian holdings are positioned for strong business fundamentals despite macro volatility.