Commentaires

Red or blue: How will the US election colour the markets?

31 octobre 2024

2024 has been a historically significant year for elections, with around half the world’s population having the opportunity to vote. We are on the eve of the main event of the year: the US election. In the Republican red corner, we have the challenger, former President Donald Trump. In the Democratic blue corner, Vice President Kamala Harris. This week’s commentary looks at potential impacts of each outcome and how stock markets have typically reacted post-election.

Industries such as energy, financial services and manufacturing that have potential for diverging directions on policy depending on the winner of this election.

Energy

Regarding energy, the current Democratic administration has been more willing to act against climate change. One would imagine VP Harris will continue this work into her term should she win, and renewable investments would remain beneficiaries of subsidies or tax breaks. Should Trump win, this support could come under pressure and preferences would shift to traditional fossil fuels in the name of energy security. Environmental regulations would loosen, permitting fast-tracked tax benefits for oil and gas firms, benefitting those with domestic exposure.

Financial services

Trump also has a history of loosening regulations in the financial industry – rolling back some of the Dodd-Frank Act to reduce regulations originally set in place to protect borrowers, for example. Should he win, this trend of deregulation may persist. However, Republicans might think twice as last year’s Silicon Valley Bank collapse was blamed by some on those same roll-backs. Harris, on the other hand, has a record of holding banks accountable during her time as California’s attorney general, advocating for a relief package to help residents impacted by foreclosures and what she considered predatory practices around student loans. She may keep up her efforts if elected.

Manufacturing

The two parties are somewhat closer aligned on manufacturing. Both publicly support US manufacturing while placing restrictive measures on China. Where the differences lie are in the industrial end markets. Trump is more vocal about China (proposing a 60% tariff on Chinese imports), but also about foreign competition in general, floating a 10% tariff on all US imports. If trade barriers do increase, domestic manufacturers who use US-based facilities to serve the US market will be at a clear advantage. “Made in the USA” is an intrinsic part of Trump’s “Make America Great Again” campaign. Universal tariffs likely mean disrupting trade flows and inflationary pressures; imported goods account for 10% of US consumer spending. US exports could also experience retaliatory measures by other countries.

Where Trump is more supportive of traditional goods and machinery (including combustion engines), Harris and the current administration have focused on electric vehicles, alternative energy, high-tech manufacturing and supply chains courtesy of the CHIPS and Science Act. Harris’ future policy on tariffs is less known, but the current administration enforced Trump’s tariffs and shifted towards protectionism. At the least, one could foresee Harris maintaining the current administration’s policies such as the $360 billion in tariffs on goods from China and increasing certain tariffs on Mexican steel and aluminum.

Taxes

The two parties have different plans for corporate taxes. Taxes are at the forefront of Trump’s economic agenda, as they were during his first term in office. Trump’s plan is to reduce the rate to 15% (from 21%) for companies with domestic production. Harris plans to raise the rate to 28%. Combined with other tax reforms, a Harris administration could see the largest increase in revenues in decades. But could it be restrictive to growth?

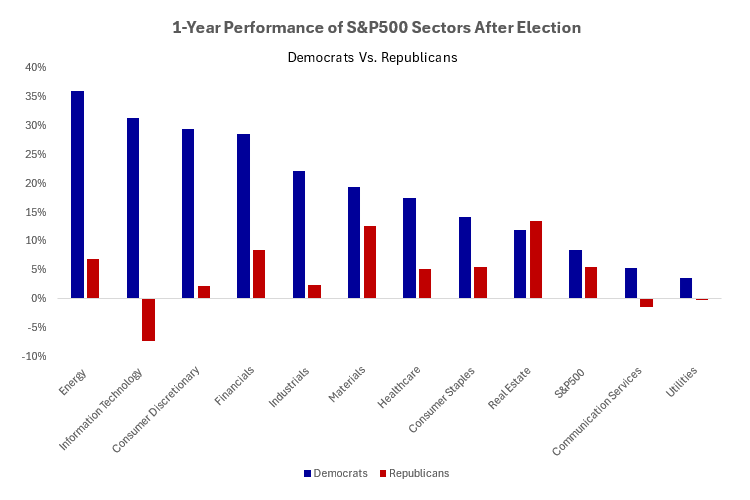

Market impacts of US election results

Historically, there is no clear connection between the election result and capital market performance in the medium- to long-term. Even the narrative of investor uncertainty leading to lower returns heading into an election has proved untrue this time around. As of October 18, the S&P 500 Index had gained 23% year-to-date, having hit 47 record highs along the way and riding the wave of six consecutive weeks with gains. Investor sentiment currently drives stocks as much as fundamentals so the details of the respective policies may not be what moves markets after election day. Returns tend to be stronger in non-election years, regardless of the election outcome, and often higher when an incumbent party is re-elected and when one party wins decisively, suggesting larger policy changes.

Source: Bloomberg. Annualized Performance is calculated using S&P 500 Level 1 GICS sector indices. Data starts in 1992 and covers eight election cycles.

With the usual caveat of historical performance not being a guarantee of future results, it is interesting to note that small caps (in this case the Russell 2000) have outperformed large (Russell 1000) by an average of 5.5% in the 3-month period after the last ten presidential elections, and by 3.3% over the subsequent 12-month period.

Diversification remains key

As in previous commentaries, we believe our diversified portfolio is especially critical in periods of uncertainty. Election outcomes can heavily influence economic policies, affecting taxation, regulations and economic reforms. These changes have the power to shape various sectors and industries in profound ways. Safeguarding your investments by diversifying across different securities and industries continues to be a wise strategy.

Quality companies that demonstrate enduring strength, guided by capable management and driven by long-term secular trends are well-equipped to weather the market’s ups and downs. Their resilience and adaptability often become key to their sustained success, offering a more grounded perspective for investors looking beyond the immediate horizon of shifting politics.