Commentary

The myth of inflation in Japan

May 5, 2022

When most countries are wrestling with rising inflation, Japan is the outlier.

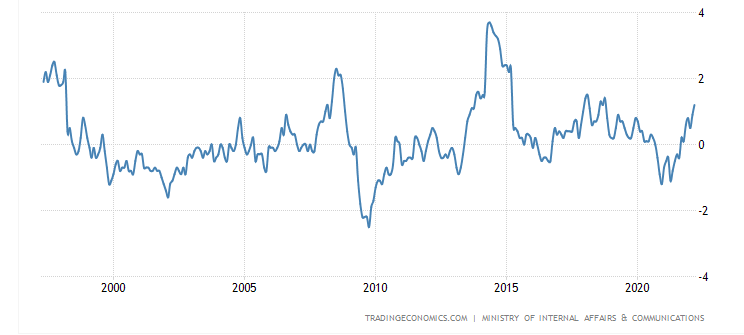

In March 2022, Japan’s consumer price index (CPI) growth was only 1.2% year-over-year, versus 8.5% in the United States (U.S.). Japan’s CPI has risen only 5.5% over the past 20 years, compared to 60% in the U.S.

Inflation rate in Japan (%)[1]

In theory, it is due to a long-term demand-deficient feedback loop.

- Expectations built up through decades of low inflation or deflation

- Weak consumer spending caused by aging population

- Firms’ caution on wage and price increases

- Stagnant wage growth constrains consumer spending

In reality, for many years, the story goes like this: Anyone under 40 years old in Japan has never really experienced rising inflation. If prices go up, consumers will spend less. Therefore, firms are reluctant to increase prices. To keep costs in control, firms keep wages stable, which does not stimulate consumer demand.

However, since September 2021, the inflation rate has been increasing, from -0.4% in August, 0.2% in September, to 1.2% in March, all due to high commodity prices. On April 26, the Bank of Japan (BOJ) reiterated its commitment to low-interest rates despite rising inflation, saying: “It is most important to support economic recovery by patiently continuing monetary easing.”

At Global Alpha, we are supportive of the BOJ’s policy. Rising inflation in Japan this year is inevitable but desirable. Looked at another way, the present inflationary trend could be an opportunity for Japan to finally escape from deflation.

All our Japanese holdings said they had raised their prices in the past year. According to the Teikoku Databank Ltd survey of 1,855 companies conducted in early April[2], 43.2% of the firms said they raised prices in April or plan to do so by the end of March 2023. When combined with the firms that have already raised prices between October and March, the percentage reaches 64.7% of the total.

The key for Japan to fight deflation is wage increases. According to data by the Organization for Economic Co-operation and Development (OECD), the average annual wage in Japan increased until 1997 to $38,395 and then flattened out. In 2020, the average Japanese workers made $38,515.

In November 2021, Japan’s new Prime Minister, Fumio Kishida, made it clear that raising wages is one of the top priorities for his economic agenda. He urged firms whose earnings have recovered to pre-pandemic levels to increase wages by 3% or more at their labour talks this spring. Prime Minister Kishida also pledged to raise the incomes of welfare workers, such as childcare workers, nurses and caregivers, by 3%, continuously.

Of course, a policy does not lead to easy solutions, considering Japan’s rigid employment culture, the large presence of part-time and contract workers, and a weak yen. The progress is yet to be seen.

Japan has been a very important market for our investments. Despite low inflation pressure and limited geopolitical risk, Japanese stocks are currently trading at an attractive valuation compared to other markets.

Forward Price/Earnings

This year, JPY against USD has weakened by over 10%. The 130 milestone was the highest in two decades. We believe the rate should revert to 100 – 110 in the coming years. Meanwhile, a weak yen benefits exporters and encourages inbound travel. As Japan reopens, we foresee “revenge spending” from in-bound travellers. In 2019, almost 32 million foreign tourists spent 4.8 trillion yen.

[1] Japan Inflation Rate – April 2022 Data – 1958-2021 Historical – May Forecast (tradingeconomics.com)

[2] Get ready to pay more: Over 40% of Japanese firms to raise prices within a year: survey – Japan Today