Commentary

Why travel offers resiliency amid a tough consumer spending outlook

February 6, 2025

When the COVID-19 lockdowns happened, it was no surprise that travel-related stocks were among the hardest hit. However, as the world emerged from the pandemic, these stocks saw an impressive recovery as people were eager to start traveling again. With tourists armed with excess savings accumulated during the pandemic, tourism and business travel rebounded, filling planes, hotels and rental cars around the globe.

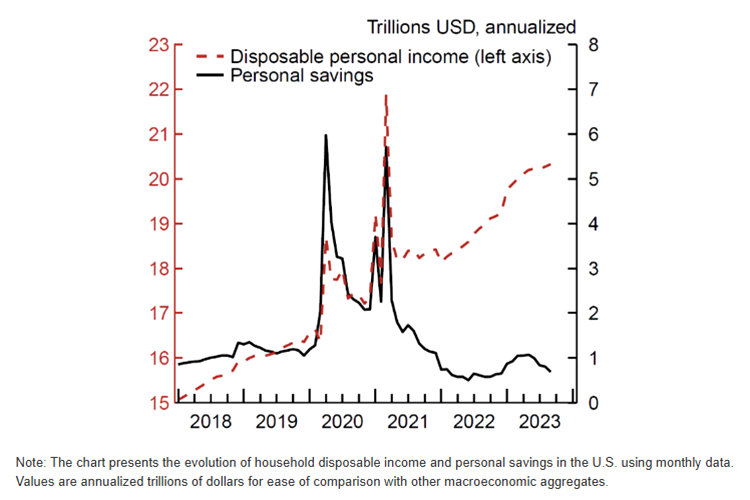

Now, fast forward to 2025, the post-pandemic recovery is behind us and the picture looks very different. Consumer spending data indicates a slowdown as higher interest rates and the potential return of inflation are putting a pinch on consumers. Even though personal savings are now back down below pre-pandemic levels, it’s important to focus on absolute wage growth, which remains strong in many regions. In other words, people are earning more, but also need to spend more just to maintain their lifestyles.

US disposable personal income and personal savings

Source: The Fed – An update on Excess Savings in Selected Advanced Economies

Source: The Fed – An update on Excess Savings in Selected Advanced Economies

With the weak outlook for consumer spending, the question arises: should we really be viewing all categories of discretionary spending the same way? In a market that’s constantly swayed by daily news and short-lived noise, it’s crucial to look past the temporary trends or “hype.” Instead, we should focus on identifying secular trends – those underlying shifts – that will remain resilient, no matter where we are in the economic cycle. From our perspective, travel and leisure is certainly an industry that will benefit from one of these secular shifts in the years to come.

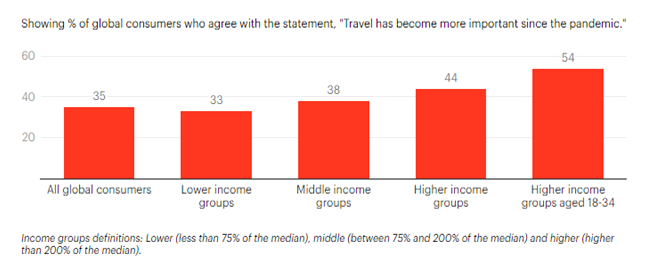

- One trend we’ve been seeing is a shift from spending on goods to a growing preference for experiences. With wage growth remaining strong across developed markets, there comes a point where consumers naturally pivot – there’s only so much you can buy, but experiences, like travel, have no limits. That’s exactly what we’re seeing play out: higher-income groups in developed markets are showing a strong appetite for travel, and consumer surveys are backing this up with increasing indications of a preference for experiences over material goods.

Young affluents show stronger appetite for travel post-pandemic

Source: Understanding affluent travel behaviors and aspirations

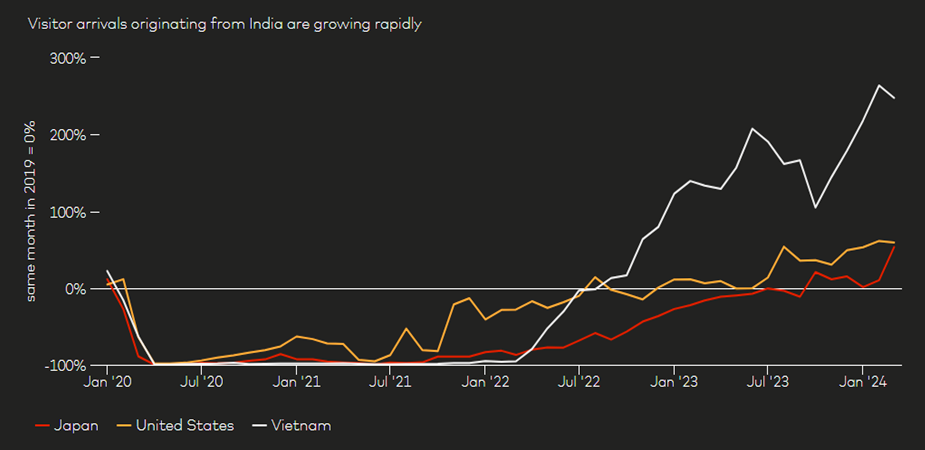

- Another key tailwind for the resilience of travel, even in a weak consumer spending environment, is the rising demand from the emerging market middle class. As some emerging economies such as India, China, Korea, Mexico and Brazil continue to develop, their expanding middle class is increasingly seeking travel experiences, both domestic and international. The World Economic Forum estimates that by 2030, Asia – home to three of the world’s five most populous countries (India, China and Indonesia) – will have 3.5 billion people in its middle class, making up two-thirds of the global middle class. Furthermore, a travel survey by Skift found that these travelers plan to allocate an average of 23% of their income to travel in the next year, with 81% stating that it remains a priority despite economic challenges.

India: Change in passenger arrivals vs. 2019 levels, by destination country

Source: Travel Trends 2024: Breaking Boundaries

- Greater mobility is another key tailwind for travel-related companies. With remote work still prevalent worldwide, we’re seeing the rise of a new generation of digital nomads – individuals who leverage flexible work arrangements to explore the world. This shift toward a “work from anywhere” model is reshaping travel patterns and creating lasting demand for the travel and leisure industry.

Given our strong conviction in travel and leisure, here are some of the key plays in our portfolios and why we hold them.

Founded in 1912 by Martin Sixt, and managed by the family since, Sixt SE (SIX2 DE) is one of the oldest car rental companies in the world. The company is headquartered in Germany and operates across more than 110 countries. It differentiates itself from competitors through its premium car offering, thanks to its German heritage and strong relationship with German carmakers. Its motto is “Don’t rent a car, rent THE car.”

After becoming a top two player in Europe, Sixt has expanded in the United States by prioritizing a presence in the busiest airports, which has yielded above average results, but has brought some challenges along with it. The key difference between the US and European car rental business models lies in the accounting of fleet ownership. In the United States, rental companies primarily assume the risk of lease or buyback agreements, meaning they bear the depreciation risk.

Sixt experienced that risk first-hand in early 2024 when the resale value of electric vehicles fell as much as 20% and the company had to book accelerated depreciation in its book which sent the stock price down close to 30% over Q2. We took that opportunity to initiate a position in this high-quality name as we expect the impact of depreciation to be short term in nature as the management has taken steps to accelerate the rotation of its fleet. We remain confident in the company’s ability to successfully execute its US expansion plans and take market share from competitors such as Hertz and Avis.

Founded in 1995, easyJet plc (EZJ UK) is one of Europe’s leading low-cost carriers (LCC), offering a pan-European point-to-point flight network at a cost advantage to legacy and charter airlines. With a strong brand recognition, the company has grown notable presence at capacity-strained airports. Unlike ultra-low-cost-carrier (ULCC) peers, easyJet differentiates itself by operating from major primary airports rather than secondary hubs, prioritizing customer experience and maintaining competitive, flexible service offerings that command significant brand loyalty from its passengers. easyJet also benefits from a streamlined cost structure and ability to rapidly adjust capacity to market conditions, giving them a competitive advantage in times of sector disruption. Additionally, the company is taking market share from traditional full-service carriers by extending its reach beyond standard short-haul flights through its easyJet Holidays business, tapping into the roughly $80 billion European package holiday market. easyJet’s focus on cost efficiency, network optimization, diversifying revenue streams and gaining market share from legacy carriers positions it as a long-term winner in European aviation.

Meliá Hotels International S.A. (MEL ES) is a leading global hospitality group founded in Spain in 1956. As the second-largest hotel group in Latin America and the third largest in Europe, Meliá has expanded to over 390 hotels across 40 countries with 63 new hotels in the pipeline. The company operates through a multi-brand portfolio spanning the premium, upscale and midscale segments. Meliá caters to a diversified mix of leisure and business travelers in key resort destinations across the Americas, Spain and EMEA. Their strategy to increasingly adopt an asset-light model – more than half of their portfolio consists of managed and franchise properties – reflects their focus on scalability and margin improvement. Meliá differentiates itself with a strong brand portfolio, a high Global Reputation Index score, and growing direct-to-consumer sales, which enhance margins and strengthen customer loyalty. With an established presence in high-growth markets, along with its ongoing upscale repositioning and expansion pipelines, the company is well positioned for continued growth.

Founded in Denver, Colorado, Samsonite International S.A. (SMSEY) is the world’s largest lifestyle bag and travel luggage company. Its broad, high-quality broad portfolio includes Samsonite, Tumi, American Tourister, Gregory, High Sierra, Kamiliant, eBags, Lipault and Hartmann, collectively sold in over 100 countries through more than 1200 company-owned stores. Samsonite’s business model is centered on brand management, product design, and marketing, with 95% of its manufacturing outsourced to a global network of around 1,500 third-party facilities.

Samsonite’s asset-light structure allows them to prioritize brand building and innovation, reflected in their eco-friendly collections and omnichannel expansion, including a fast-growing e-commerce segment. The company is well positioned compared to its peers thanks to its scale-driven brand power and global presence resulting in a strong 17% market share of a roughly $22 billion luggage market. Additionally, their focus on cost control and supply-chain diversification reduces tariff risk and further supports margins, strengthening their position to achieve sustainable long-term growth.