Commentary

Updates from Brazil and Mexico: Rates, politics and trading

October 2, 2025

During a research trip to São Paulo this summer, our team met with the management teams of some of our holdings, with prospective investments and with local investors. We observed that consumer demand in Brazil is stronger than expected, particularly in higher-end categories. Companies we like such as Vivara Participações S.A. (VIVA3 SA) and Track & Field Co S.A. (TFCO4 SA) benefit from this consumer strength and offer a compelling risk reward given where these stocks traded during beginning of the year.

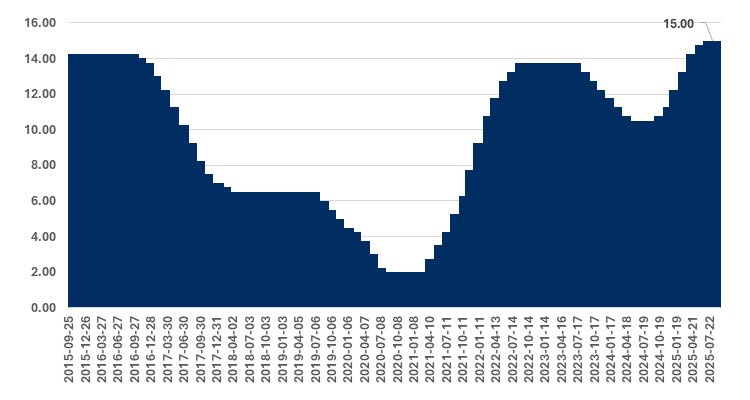

Local market behaviour remains distinctly short term, with high turnover and a focus on the next-quarter results. This is largely driven by the elevated Selic policy rate, currently at 15%, which leads investors to assess opportunities on an absolute-return basis rather than seeking alpha. With inflation near 5%, real yields approach 10%, creating a persuasive risk-free alternative that diverts capital from equities. In turn, local equity managers are adjusting their styles to retain AUM.

Banco Central do Brasil Target for Federal Funds rate (Selic)

Source: Banco central do Brasil

These dynamics reinforce our long-term approach: concentrating on high-quality businesses with durable earnings power and consistent EPS expansion. Looking ahead, with elections approaching and potential rate cuts on the horizon, we expect a reallocation of flows from fixed income back into equities, benefiting companies with strong fundamentals and clear earnings visibility.

Key players in Brazil’s political landscape

Brazil’s political landscape is already taking shape as the country heads toward the 2026 elections. One of the most significant developments is the exclusion of Jair Bolsonaro from contention. His ineligibility through 2030, reinforced by a conviction earlier this month, effectively removes the most polarizing figure on the right. In his absence, the centre-right governor of São Paulo, Tarcísio de Freitas, is emerging as the most likely challenger to President Luiz Inácio Lula da Silva (also known as “Lula”) in a potential second-round runoff. This dynamic sets up a more conventional contest between a centre-left incumbent and a pragmatic, reform-minded conservative.

For Lula, the current year has been a test of political resilience. His approval ratings hit a low point of around 24% in February 2025, but have since rebounded modestly, reaching roughly 33% by September according to Datafolha surveys. The recovery suggests some stability, though his support remains fragile, reflecting persistent dissatisfaction with the pace of economic recovery and concerns about fiscal policy. Nevertheless, the directional improvement offers the president some breathing room as he navigates the second half of his term.

From the perspective of markets, the electoral outlook carries important implications. A Lula re-election would imply continuity in the Workers’ Party approach: a more active state role in economic management, coupled with efforts to demonstrate adherence to Brazil’s new fiscal framework. Investor reaction would likely hinge on whether the government can maintain a credible path to primary balance and on its stance toward state-controlled enterprises such as Petrobras, where governance remains a focal concern. By contrast, a victory for a centre-right figure like Freitas would be interpreted as a more reformist and privatization-friendly outcome. Such a scenario could lower perceived political risk, reduce risk premia and prove supportive for equities and local rates markets.

Mexico rates, USMCA and tariffs

Headline inflation in Mexico remained relatively stable, with the Consumer Price Index (CPI) registering a 3.57% year-over-year increase in August. Preliminary mid-September data suggests a slight acceleration to approximately 3.7%. Inflation expectations continue to trend downward. The Bank of Mexico’s (Banxico) August private-sector survey shows a further decline in median inflation forecasts for both 2025 and 2026, signaling growing confidence in price stability.

On September 25, Banxico lowered its policy rate to 7.50%, executing a 25 basis point cut. The decision was not unanimous, reflecting differing views within the board. Forward guidance remains cautious, as core inflation is decelerating only gradually. Reuters notes that while the easing cycle supports domestic demand and longer-term fixed income instruments, external factors – particularly the pace of US Federal Reserve rate cuts or potential tariff shocks – will ultimately drive risk premiums in Mexican assets.

In 2026, the United States–Mexico–Canada Agreement (USMCA) is scheduled for its first mandatory joint review. At that point, the three countries must decide whether to extend the agreement for another 16 years, renegotiate its terms or allow it to transition into annual reviews. The outcome will directly affect trade certainty and tariff exposure in North America. Currently, approximately half of Mexico’s exports to the United States do not qualify under USMCA’s origin requirements and are therefore vulnerable to a 25% US tariff. Goods meeting the agreement’s rules of origin continue to benefit from duty-free treatment, but non-compliant products face higher costs and stricter enforcement.

In parallel, Mexico has recently imposed tariffs of between 10–50% on a wide range of imports from China, including auto parts, textiles, steel and consumer goods. This move underscores Mexico’s effort to shield domestic industries from low-cost Chinese competition, but also adds a layer of complexity to supply-chain strategies for companies operating across the region.

The 2026 review will thus be a critical inflection point: it could either reaffirm the stability of North American trade or introduce uncertainty through renegotiation and tariff escalation.