Commentary

One person’s trash is another’s treasure

June 20, 2024

When one thinks of high-return investments, the waste management sector rarely comes to mind. It’s not as exciting as tech or biotechnology companies. Yet, the waste services industry has captured the attention of some of the world’s most sophisticated investors. For instance, the Gates Foundation owns over 35 million shares of Waste Management, the largest waste service company in the United States, making it one of the foundation’s top holdings. Private equity funds also have a keen interest in this sector, with those specializing in environmental services amassing more than $1.3 trillion globally, according to PitchBook.

Global dry powder: private equity funds seeking investments in environmental services (in billions)

Source: PitchBook.

Source: PitchBook.

So, what makes the waste management business so attractive to some investors?

The sheer size and growth potential of the market. Globally, more than two billion tons of municipal solid waste are generated annually. To visualize this, if packed into standard shipping containers and placed end-to-end, this waste would circle the Earth 25 times, or to the moon and back. On top of municipal waste, human activity generates significant amounts of agricultural, construction, industrial and healthcare waste. The global waste management market was valued at $1.3 trillion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 5.4% until 2030, reaching $1.96 trillion.

Recession-resilient business model and high entry barrier. Waste management is a fundamental service in modern society. Every day, millions of tons of waste are generated, requiring efficient collection, treatment and disposal. This ongoing need makes waste management companies indispensable, ensuring a stable demand regardless of economic conditions. These companies typically generate strong cash flows, high margins and significant return on capital. Long-term contracts with municipalities and businesses provide predictable revenue streams. Moreover, high entry barriers associated with sizable upfront investment and stringent regulations deter newcomers, giving existing players pricing power and reducing competitive pressures. This stability translates into reliable revenue streams, making the sector attractive for long-term investors.

At Global Alpha, we have identified numerous promising investment opportunities within the waste services sector over the years. Here are some examples:

- Casella Waste Systems (CWST US) is a regional player providing integrated waste services, with a strong focus on the US Northeast and Mid-Atlantic regions. The company benefits from its strategic positioning in the capacity-constrained Northeast market, allowing it to capitalize on pricing power and opportunities for growth through M&A. The company also emphasizes operational optimization to enhance margins and efficiency.

- Befesa (BFSA GY) is the world’s leading recycler for steel dust and aluminum, with recycling facilities across Europe, Asia and North America. The company has over 50% market share in Europe and is a first mover in China for steel-dust recycling. With increasing regulatory mandates requiring decarbonizing steel production, Befesa is well-positioned to capture the volume growth with a well-defined capacity plan.

- Daiseki (9793 JP) is Japan’s largest liquid waste processor, including waste oil, wastewater and sludge. Its recycling technologies can treat waste oil to produce recycled lubricating oil, heavy oil and supplemental fuels. Demand for recycled oil is rising as Daiseki’s clients seek to reduce their carbon footprint.

- ARE Holdings (5857 JP) is the world’s largest precious metals refiner. The company collects, recycles and refines precious metals, including gold, silver, platinum and palladium from dental, electronics and jewelry materials. The carbon footprint of recycled silver is roughly one-third of mined silver. Recycling gold emits less than 1% of emissions than mining new gold. Many industry players, such as Prada, Tiffany, Cartier and Pandora, now use recycled metals.

- TRE Holdings (9427 JP) is one of the leading waste treatment and recycling companies in Japan, specializing in handling construction waste and waste metals from automobile, home appliances and industrial sectors. It has over 20% market share in the construction industry and recycling schemes with auto makers and home appliance manufacturers. The company also has renewable energy businesses that use recycled wood from its own operations as fuel for biomass power generation.

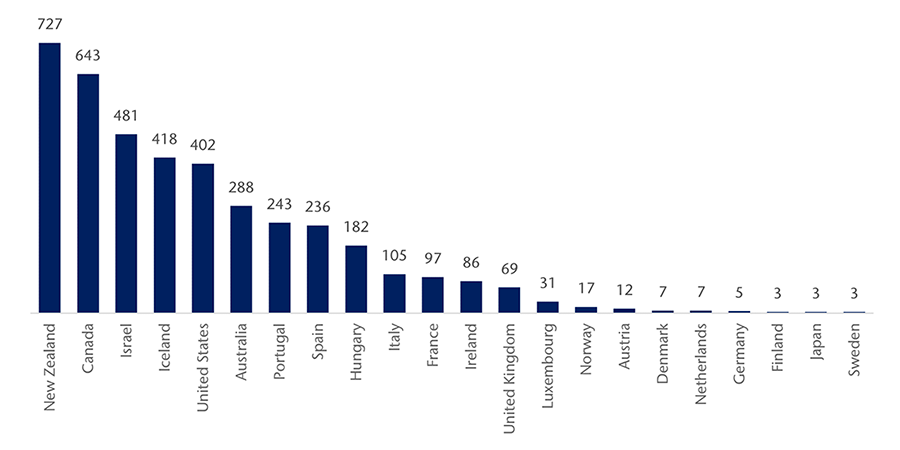

When it comes to waste management, Japan is known for its rigorous waste sorting and disposal practices. The country faces a challenge with limited landfill capacity. Existing landfill sites have remaining capacity of 96.66 million cubic meters, projected to reach full capacity in 23 years, so Japan tries to minimize garbage through efficient sorting and processing. That explains why Japan has such low landfill waste per capital compared to other economies.

Global landfill waste generated per capita 2022, by select countries (in kilograms)

Source: Statista.

Source: Statista.

Daiei Kankyo (9336 JP), a name added in our portfolios in a recent quarter, is a Kansai-based waste disposal company that offers one-stop services from collection, transport and intermediate processing, to final disposal. The company has top share in the final disposal market among private-sector players, accounting for approximately 11% of Japan’s total landfill capacity. The final disposal business is extremely difficult for new players to enter because of the strengthened regulatory processes and environmental concerns by local communities. Only companies with a strong track record and reputation can possibly get a permit and expand their capacity. Additionally, it takes six to seven years to open a new facility. This lengthy process further increases the barriers to entry, ensuring stable volume growth and strong pricing power for incumbents. That’s why Daiei Kankyo boasts the highest margin among its waste management peers in Japan. Over the years, the company has diversified into recycling, soil remediation and electricity generation businesses to provide a total solution to its clients.

In contrast to other markets, Japan’s waste management industry is more fragmented, with the four players accounting for only 4.2% of the market, compared to 40% to 50% of the US market, which allows ample M&A opportunities. Daiei Kankyo has acquired over 20 companies since its founding in 1979, typically at EV/EBITDA multiples of 3x to 5x. M&A will remain a growth driver in the coming years.

Another driver for the company is public-private partnerships (PPP). Many Japanese local municipalities struggle with handling household waste due to a declining population and labour shortages and have started working with private players. Daiei Kankyo pioneered PPP contracts where the plant will be built, owned and operated by Daiei Kankyo, and municipalities will pay waste treatment fees once operational. So far, the company has won three orders and expects to win 12 by 2030.

Turning waste into wealth

While only a small portion of waste is recycled, global innovators and industry leaders are finding new ways to turn waste into sustainable materials or fuels. The potential for these innovations to convert waste streams – currently incinerated or buried – into valuable resources is promising for the future.