Commentary

K-series part 1: Shipbuilding in LNG carriers and dual-fuel vessels

December 5, 2024

Source: Hyundai Heavy Industries

Last month, we visited Korea (South, not North) which remains in the “Emerging Markets” indices. We visited to conduct due diligence on existing and prospective holdings, attend a conference and meet with and learn from local asset managers who share the same approach to investing as us.

From the Miracle on the Han River to K-everything

From the ruins of the Korean War (1950 – 1953), Korea emerged to become the tenth largest economy in the world in 2005. Dubbed “the Miracle on the Han River,” Korea’s GDP grew from USD1.3 billion (GDP per capita of USD67) immediately after the war to over USD1.7 trillion (GDP per capita of over USD33,000) 70 years later in 2023. Continuous investment in technology and human capital has been a driving force behind the economic development. According to Organisation for Economic Co-operation and Development’s (OECD) latest publication on R&D spending as a percentage of GDP data, Korea (5.2%) ranked second only to Israel (6.0%) and higher than the United States (ranked third with 3.6%) in 2022.

First used to denote Korean pop culture (K-pop) and Korean drama (K-drama), the use of the “K-” prefix to introduce anything Korean to the outside world has spread to K-food (Korean BBQ, Buldak ramen), K-beauty (Beauty of Joseon, Anua, Cosrx), K-defense (K2 tank, K9 artillery), etc. What is interesting is that given the diversity of industries represented in the Korean Stock Exchange, these K-themes present potential investment opportunities. In this week’s commentary, we take a closer look at one of the themes that has been gaining traction among the local asset managers: K-shipbuilding.

Korea as a global shipbuilding powerhouse

Korea, China and Japan dominate the global shipbuilding scene, with combined market share of 91% in terms of Compensated Gross Tonnage (CGT) in 2023. China accounted for 51% and leads the world in dry bulks, tankers and containerships as the world’s largest importer of commodities. Korea, which came second with 26% share, has differentiated by prioritizing high-value ship orders (liquified natural gas carriers (LNG carriers), gas carriers and drill ships) given its cost disadvantage versus China. When we visited HD Hyundai Heavy Industries (329180 KS)’s shipyard in Ulsan – which is the largest shipyard in the world – we were able to see with our own eyes that of the ten fully occupied dry docks, six or seven of them had LNG carriers under construction. In 2022, the world saw an unprecedented number of orders for LNG carriers. One hundred and sixty-three LNG carriers were ordered in 2022, up 117% year-over-year and nearly five times the prior 20-year average of 34. Korean shipyards won orders for 121 LNG carriers or 74% of total.

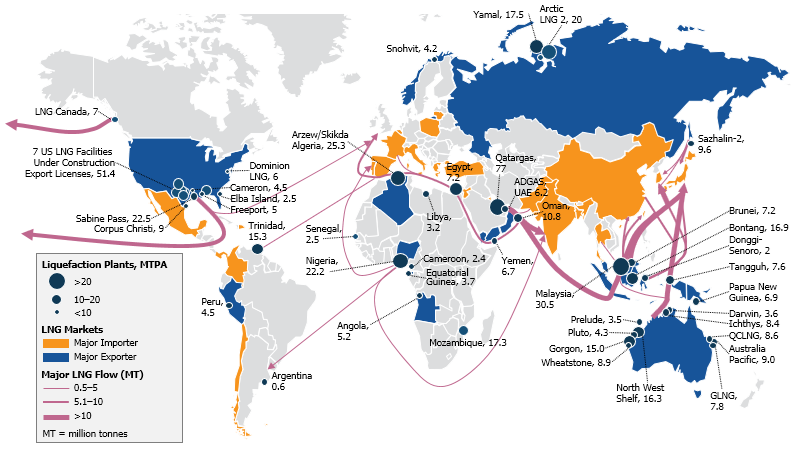

LNG is widely regarded as a “bridge fuel” to smooth the transition to net zero. Over the years, the United States has emerged as a major exporter of LNG, joining the ranks of the Middle East and Australia as top exporters of LNG. The demand for LNG is mostly found in Asia and Europe, sparking demand for LNG carriers that can transport the liquid across the seas.

Source: LNG export & import shipping routes. Incorrys, used with permission.

LNG is also increasingly being used to power ships (as dual fuel), and this is driven by the strengthening greenhouse gas (GHG) emission regulations in the maritime industry. On January 1, 2020, the International Maritime Organization’s rule (known as IMO 2020) to limit the sulphur content in the fuel oil used to power ships came into force. Last year, the IMO unanimously agreed to reach net-zero GHG emissions from international shipping by 2050. This year, the EU ETS (EU Emissions Trading System) introduced the first ever carbon tax for ships entering and exiting EU ports.

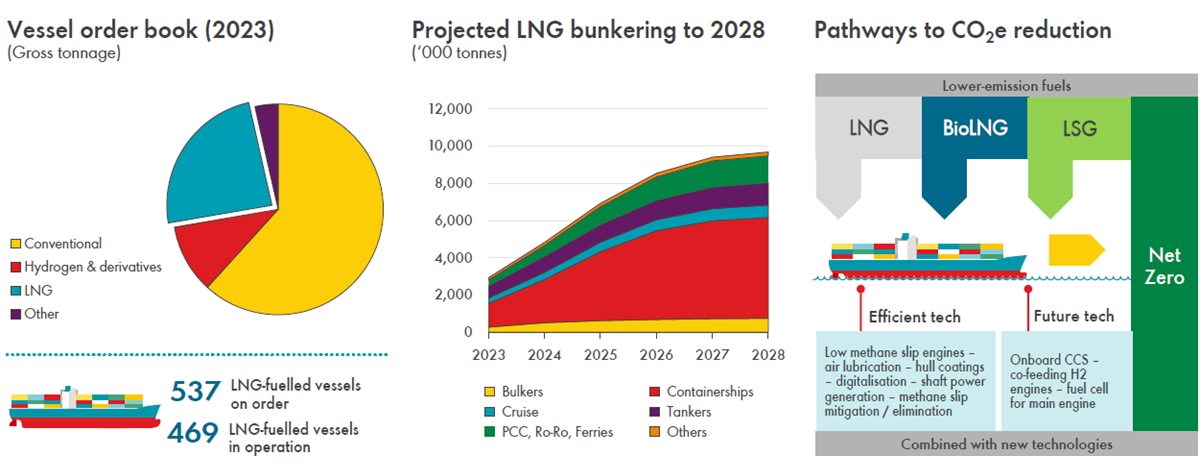

Against this backdrop of strengthening GHG emission regulations in vessels, Shell projects LNG bunkering to increase as more containerships are expected to run on LNG. We met with senior engineers from Samsung Heavy Industries (010140 KS) and HD Hyundai Mipo (010620 KS) during our trip and learned about how the regulations are driving the Korean shipyards to develop next generation ships powered by LNG, ammonia and liquified hydrogen. HD Hyundai Mipo expects LNG bunkering to remain the primary fuel choice until 2040, after which ammonia is expected to take over. Year to date, of the eight orders for LNG bunkering vessels, HD Hyundai Mipo alone won three.

Source: Shell interpretation of Clarksons Research, DNV. Shell LNG Outlook 2024.

Investment spotlight: Dongsung Finetec

Korean shipyards (including Hanwha Ocean (042660 KS) not mentioned above) offer investment opportunities to capitalize on this long-term trend of increasing demand for LNG and vessels powered by alternative energy sources. However, their market caps are either above our limit or closer to the limit offering limited upside. At Global Alpha, we study an industry’s supply/value chain to identify how and where else the value is captured in the ecosystem.

Dongsung Finetec (033500 KS) is a Korean manufacturer of Mark III (licensed from GTT) membrane type cargo containment system (CCS) that is used to store LNG. The company serves both the Korean and Chinese shipyards and is one of only two companies (duopoly with 50% market share) that manufactures the CCS in the Korean LNG carrier supply chain. The company also manufactures LNG fuel tanks for ships using LNG as dual fuel and for LNG bunkering vessels and is currently developing an ammonia fuel tank.

When we invested in the company in late October, its share price had not reflected the company’s order backlog – which amounted to over four times the company’s 2023 revenue on the back of record LNG carrier order wins by the Korean shipyards – or the increased production capacity to convert more of the backlog to revenue. Trading at the time at only mid to high single digit price to forward earnings and against the backdrop of structural growth in demand for its CCS and fuel tank, we knew we had found a mispriced opportunity.