Commentary

Japan in the 80s and the US today – bubbles in both cases?

August 8, 2024

Can the Japanese bubble of the 80s serve as a warning for the US real estate and stock markets today?

The mid to late-80s were the years of Japan’s “bubble economy”. A time when the country was at its economic peak. A time when everything was made in Japan and Japanese companies would conquer the world. A time when the US put tariffs on Japanese goods and engineered a currency accord that meant a rapid appreciation of the yen.

Consider a few historical economic facts about Japan around that time.

- At the end of 1989, the Nikkei 225 stock market reached 39,000, a historic high it would only see again in 2024.

- The Japanese property market was worth four times more than the US property market. It was rumoured (although not for sale) that the land on which the Japanese emperor’s imperial palace sits was worth more than the entire state of California.

- By 1989, the market capitalization as a percentage of GDP was 151%, while it was 62% in the US.

- Over the same time period, Japan represented 42% of global equity markets. This was almost 18% of the global economy, or approximately 71% of that of the United States.

Those were the heydays for Japan. And then came the decline.

So, what caused the crash of both real estate and stock market? There are several reasons, but two stand out:

- First was the Bank of Japan (“BOJ”) was too slow in tightening, creating an asset bubble. One reason given for the reluctance of the BOJ was the US stock market crash in October 1987 (aka Black Monday).

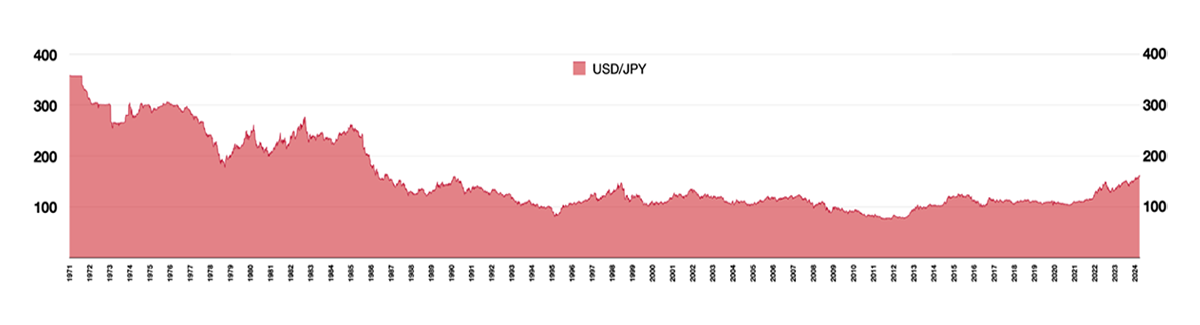

- Second was the rapid appreciation of the yen following the Plaza Accord of September 1985 when most major economies agreed to depreciate the US dollar.

US dollar / Japanese yen exchange rate

Source: Bank of Japan

Source: Bank of Japan

Now, let’s look at the US in the 2020s.

The relentless rise and outperformance of the US stock market(s) over the last few years has led many to believe it is entirely justified and pointless to diversify beyond the US market – but that narrow perspective comes at a cost.

Let’s review a few facts, keeping in mind our description of Japan’s bubble economy:

- The US stock market is now 65% of the MSCI ACWI (All Country World Index), while the US economy is only 25% of the global economy.

- By sharp contrast, the second largest country in MSCI ACWI is Japan, with a weight of 5%. Its economy is about 4.5% of the global economy.

- The weight of China, the second largest economy with 18% of global GDP, is only 2.6% of the MSCI ACWI. That is less than the market cap of Alphabet (Google). Indeed, the individual market cap of Apple, Microsoft and Nvidia are all higher than any single stock market in the world, except Japan.

So, is the US market in a bubble at the moment?

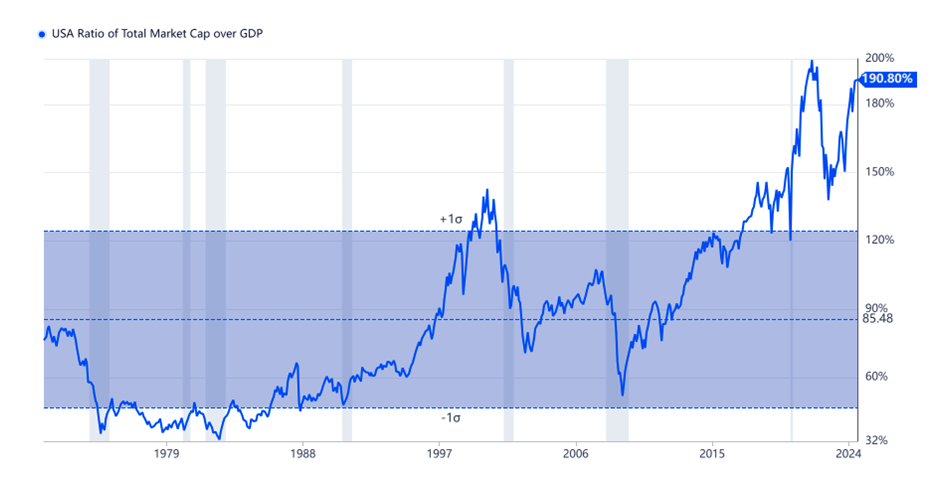

A favourite bubble indicator used by Warren Buffet, is the ratio of the US total market cap over GDP. As seen in the following chart, that ratio is currently around 190% (and helps explain Warren’s approximate $300B cash pile).

US ratio of total market cap over GDP

Source: public

Source: public

As a comparison, the same market-to-GDP metric applied to China is 61%, 48% for Germany, and 71% for the UK.

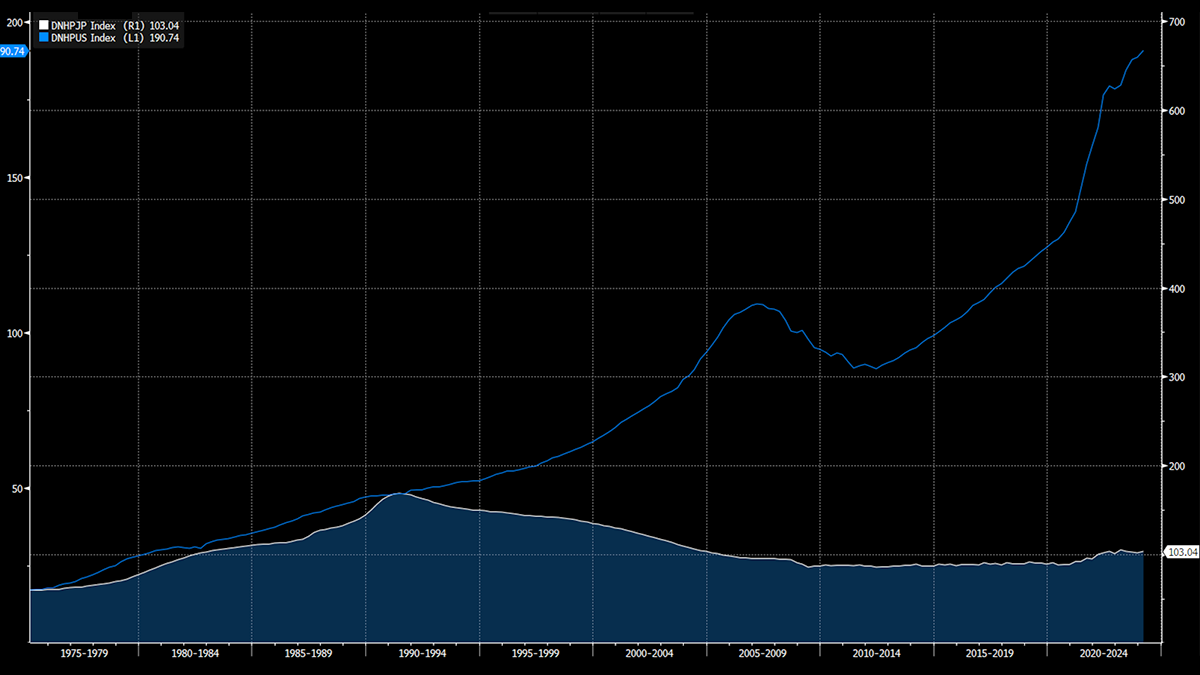

Japanese vs US stock market: 1975-2024

Source: Dallas Federal Reserve

Moving to real estate, US housing prices are at an all-time high, and housing affordability has hit the lowest level on record this month.

US vs Japanese housing prices: 1975-2024

Source: Dallas Federal Reserve

This commentary is not meant to signal an imminent crash of US house prices or stock market. Rather, it is just meant to show how we are in uncharted territory, and how looking at what happened to the Japanese economy could help navigate the present US economy.

Consider some events from the past few years:

- Did the decision to raise rates come too late, potentially lead to an inflated asset bubble?

- Has the US dollar shown signs of strengthening against other currencies?

- Is the fiscal deficit in the US inflationary?

- Is the US resorting to tariffs?

Arguably, the answers to all the above would be “Yes”. This begs the question – should we consider the similar historical context of both economies?

Given what I’ve said earlier on the narrow perspective of investors flooding the US market in the last year, there are many troubling signs on the horizon, while there is continued growth in the US market, it would be prudent to consider diversification – now more than ever.

And as a conclusion, here is a graph of the S&P 500 in a past period.

S&P 500 Index: 1928-1949

Source: public

Source: public