Commentary

Don’t discount the discounters

June 5, 2025

One of the greatest disruptions in recent years to the global grocery market has been the rising popularity of discount retailers like Lidl and Aldi. The two German-based supermarket chains have expanded rapidly, challenging the incumbent grocery players to rethink their strategies.

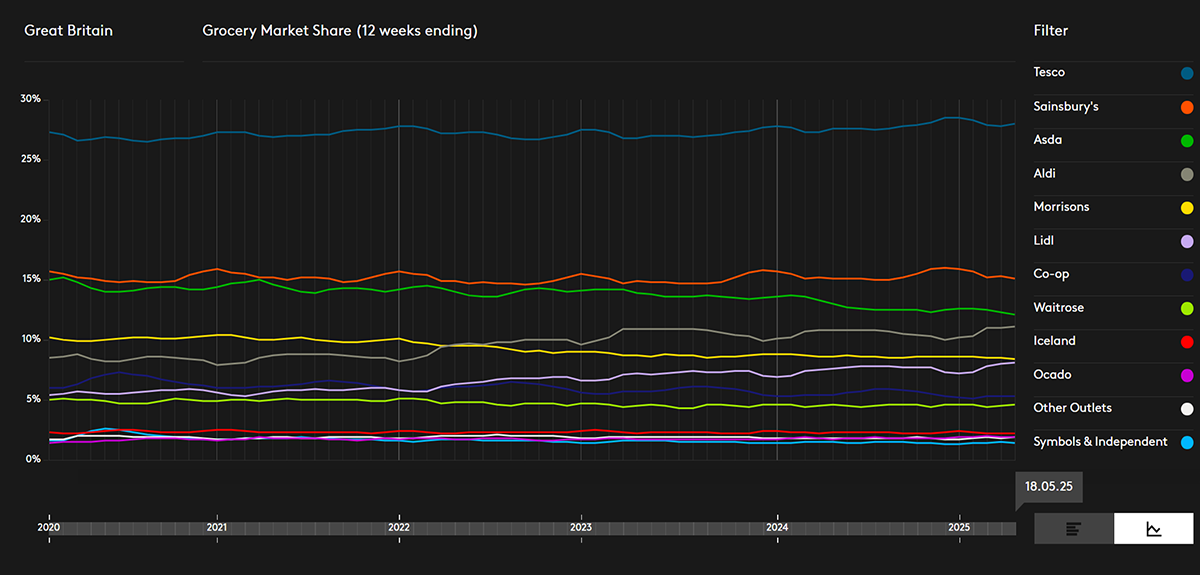

Lidl and Aldi have consistently taken market share in key markets. In the United States, Lidl and Aldi had a combined market share of 10% in 2024. It is a similar story in the UK where the two now account for around 18% of the grocery market, up from just 4% in 2008.

Source: Grocery Market Share – Kantar

The recipe for their massive success is well known: a low-cost business model that aims to offer customers high-quality products at lower prices compared to traditional grocery chains.

The Global Alpha team recently added B&M European Value Retail SA (BME LN) to the portfolio to gain exposure to the discount retailer trend. B&M is the UK’s leading variety goods value retailer. The main brand, B&M itself, offers grocery, fast-moving consumer goods (FMCG) and general merchandise in a variety of stores, located in out-of-town, suburban retail parks or, more recently, town centers.

B&M has a similar playbook to when Aldi and Lidl first entered the UK market, with an everyday-low-cost operating model leading to an everyday-low-price offering. Where B&M differs from Aldi and Lidl is that they offer a more targeted range of branded convenience grocery products such as shelf-stable food, soft drinks, confectionery and alcohol, in addition to FMCG categories such as toiletries and cleaning products.

Aldi and Lidl’s success has been built largely on the back of private-label products. Aldi stocks its stores with around 90% private-label products across all categories. B&M sells the well-known brands that families have been accustomed to using for years, sometimes generations, often at a 15% to 20% discount to the traditional grocer. B&M can do this as they have a disciplined approach to which stock keeping units (SKUs) they keep in store. By focusing on the top sellers, the volume demanded for a particular SKU creates buying power and more advantageous buying terms.

An easy way to visualize what B&M offers is to think of the middle aisles of a supermarket. B&M’s offering should be seen as complementary to, rather than a substitute for, a fresh grocery shop. Management has even communicated that some of their better performing stores are located next to an Aldi or Lidl; a customer will shop for fresh or frozen items in Aldi or Lidl, then completes the shopping in a B&M store.

In addition to the focused grocery offering, B&M offers higher-ticket general merchandise products that cover product categories such as homewares, electrical, gardening, toys and DIY. As customers wander the aisles, there is a “treasure hunt” browsing experience that often leads to impulse purchases. The general merchandise products are more aligned to seasonal trading patterns – the spring/summer seasons will see more garden and outdoor living products, whereas the autumn/winter seasons will see more toys and Christmas decorations.

The low-cost sourcing discipline is key to maintaining a price advantage over the competition. The reduced complexity of the supply chain helps keep costs low. Selling no fresh or frozen products means no need for refrigeration or freezers either on the shop floor or in storage areas. There is also less waste and the need to reduce prices to clear fresh produce approaching expiration date. B&M does not have an online or click-and-collect operation. As well as being historically lower profitability than offline purchases, it also adds a layer of complexity.

When shopping for groceries, a little bit of planning can go a long way. B&M has increasingly become a part of the weekly routine for budget-conscious shoppers. B&M will be a long-term beneficiary of the discount retailer trend and shows that growth can be found in “value.”

Like-for-like growth is typically highly profitable and the most desirable form of growth. B&M themselves state that 1% in LFL sales growth is the same as opening over seven new stores, but without the associated capex or increase in fixed costs. This can be achieved by taking a bigger share in existing catchment areas by offering a great value proposition. But B&M has a parallel growth strategy. The company expects to increase store numbers by at least 60% to reach no less than 1,200 B&M stores in the UK. This represents a decade-long growth runway at the current pace of openings. The new stores tend to be larger and often with a garden centre attached, so underlying sales are expected to grow ahead of the 60% increase in stores. More stores equal more volumes and, in turn, greater benefits to buying and productivity.

France is another avenue of growth. B&M entered the French market in 2018 via an acquisition, but all stores now operate under the B&M fascia. B&M currently operates 124 stores in France which has a population like that of the UK where B&M is targeting over 1,200 stores. Despite the upside potential in new stores, the pace of the rollout is slower than in the UK, opening around 10 new stores per year, due to a focus on profitable growth rather than rapid expansion.

The traditional top four UK grocers are not idly standing by while the discounters take market share. Asda was the first to come out and promise price cuts to be more competitive. Tesco PLC (TSCO LN), the market leader, expects a significant reduction in profitability owing to “a very competitive market.” J Sainsbury PLC (SBRY LN) then announced price cuts to compete with Tesco and Asda.

Price war or not, discount retailers are here to stay, and we believe B&M has a long cycle of growth ahead.