Commentary

Capstone Copper: Positioned to benefit from a structurally tight copper market

February 12, 2026

Chile’s 2025 presidential election marked a meaningful political inflection, with markets interpreting the outcome as a shift toward a more pro-business, market-oriented policy framework focused on restoring economic growth and encouraging private investment. The incoming administration has emphasized fiscal discipline, regulatory clarity and the strategic importance of export-oriented sectors – particularly copper – in driving medium-term economic expansion.

For the mining sector, this shift points to clearer permitting processes, a more pragmatic stance toward private capital and improved project visibility, all of which are especially relevant for long-life assets requiring sustained investment. Against a backdrop of structurally rising global copper demand – driven by electrification, grid expansion and the energy infrastructure needed to support AI-related data centre growth – this political realignment strengthens the case for selective exposure to high-quality copper producers.

Capstone Copper Corp. (CS TSE) is well positioned to benefit from this environment, with approximately two-thirds of consolidated copper production generated in Chile, providing direct leverage to a more constructive domestic policy backdrop. The company is executing a district-scale growth strategy targeting a ~70% increase in annual copper production to approximately 400 ktpa, driven by long-life Chilean assets and capital-efficient brownfield expansions. Near-term growth is led by the Mantoverde Optimized expansion, expected to deliver an incremental ~20ktpa of copper with declining unit costs, while the fully permitted Santo Domingo project represents a transformational medium-term opportunity with a sanctioning decision expected in H2 2026. Supported by more than $1 billion in available liquidity and net leverage of approximately 0.9x EBITDA (TTM), Capstone is well positioned to translate a supportive policy environment into improved execution, cash flow growth and valuation upside.

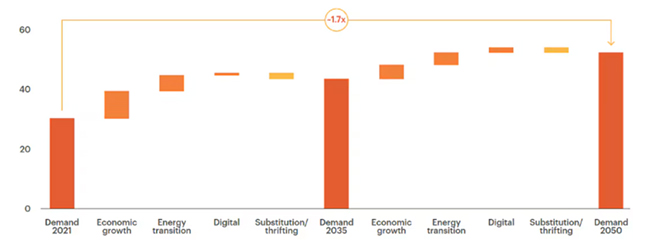

Global copper demand is poised for significant growth over the coming decades, with BHP projecting a roughly 70% increase to more than 50 million tonnes annually by 2050, up from around 31 Mt as of 2021.

Copper demand projected to grow ~70% through to 2050…

(Copper demand by key theme, Mt)

Source: “BHP Insights: how copper will shape our future,” BHP

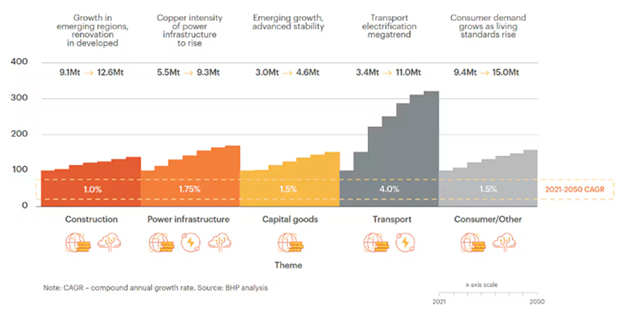

This surge is driven by a combination of traditional economic expansion, as developing economies electrify and improve living standards, and newer demand sources tied to the energy transition and digitalization. Technologies such as electric vehicles, renewable power infrastructure and data centres – all of which are copper-intensive – are central to this trend, fueling higher material requirements even as substitution and efficiency improvements evolve.

…an average of 2% per year*

(Copper demand by end-use sector, indexed to 2021)

Source: “BHP Insights: how copper will shape our future,” BHP

These dynamics favour producers with scalable assets, permitted growth projects and balance sheet flexibility. In this context, Capstone Copper is well positioned to benefit from supportive domestic policy and increased demand for copper, with an opportunity to increase valuation and sustain cash flow through disciplined execution.