Commentary

What goes up must come down or find its ground

October 27, 2022

Recently, we have seen a pullback in commodity prices after the rally they experienced earlier in the summer. As many global economies are forecasted to enter recessionary environments, the demand trajectory for commodities remains uncertain. Over the longer time horizon, we believe some commodities will outperform others due to resilient demand, despite short term volatility. This week, we would like to highlight one metal that we are closely monitoring.

Following the general direction of metal prices this year, copper is down a little under 20% year to date, according to Bloomberg. The recent down trend in copper prices has mainly been attributed to the slowdown in Chinese demand. Economic doubts in the region and many other factors have been attributed to the disruption in the Chinese economy.

The troubles started this summer when the country suffered its worst heatwave in years. Being one of the regions most vulnerable to physical stress, the heatwave in China resulted in many energy generation sources going offline, causing widespread power shortages. Additionally, the country continues to keep tight COVID controls in place, with no end in sight for their zero-COVID policy. As cases spike in certain regions, they have not shied away from locking down affected areas. Finally, Xi Jinping’s political agenda to push greater state control at the expense of the private sector growth cast questions on what rate of GDP growth the country can actually achieve.

With the rapid acceleration of the Chinese economy in the last decade, their demand for copper followed suit. The outsourcing trend accelerated in the 2000s further bolstered demand in the region. China currently accounts for 53% of the global copper demand, an increase from 38% in 2010. So, it is no surprise that downgrades in the speed of their economic development have caused a nervous sell off in the copper markets.

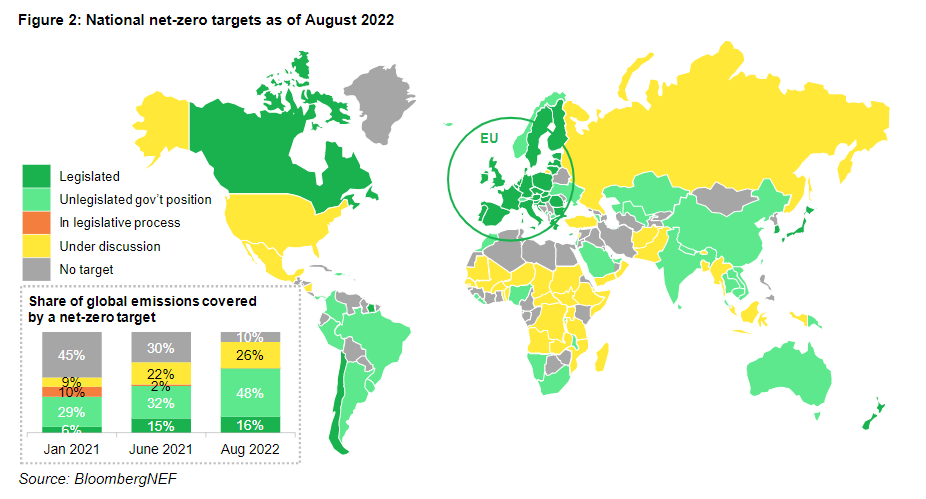

Traditionally, copper has been highly correlated to economic growth as it is an important material for construction, consumer durables, industrial equipment and ventilation and air conditioning. This type of demand for copper is called traditional demand. We are now seeing a more prominent demand driver for copper emerge, and it stems from the energy transition. Countries committing to net zero goals and setting strategies to achieve these ambitious targets will give copper demand an additional boost. Over 50% of countries around the world have net zero targets. Most are not yet legislated, but momentum is increasing as many feel the firsthand effects of climate change.

Energy transition enabling technologies are highly reliant on copper. For instance, electric vehicles require three times as much copper as internal combustion engine cars. Additionally, with wind and solar becoming more widely adopted energy generation sources, transmission and distribution lines require an increasing amount of the metal as well. These transport and infrastructure needs will experience a 3.9% compounded annual growth rate between now and 2040, contributing to an overall copper demand growth of 53%.

The supply side, however, is expected to experience a squeeze. Mines have been seeing declining copper grades. Additionally, new mine commissioning takes up to ten years from initial phase to operation as environmental permits, financing and operations are all lengthy processes. Other sources of copper supply will be critical to meet the roughly 14 million tons shortage (BNEF). Solutions such as copper recycling and yield improvement technologies will play a key role.

Aurubis (NDA GR)

We currently hold Aurubis in our portfolio, a world leading copper smelter and refiner. The company is also one of the largest copper recyclers in the world. As was the case with many European companies, they experienced rising energy costs as a result of the war in Ukraine, weighing on their performance. However, we strongly believe in the positive long-term trend for the industry. Aurubis is extremely well positioned to benefit from the energy transition. Their main smelter is one of the most efficient in the world and the company outperforms its peer group in terms of GHG emission intensity. Suppliers with better performance should benefit as more and more emphasis is put on managing Scope 3 emissions. Additionally, their recycling division is bound to thrive as regulations impose higher recycling rates and natural copper deposits continue to decline.

We believe that given the strong demand, copper prices should find a floor and stabilize, experiencing a more favorable pricing environment than other metals.