Commentary

India: Our EM Queen

October 13, 2022

“It is far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

– Warren Buffet

“Anticipate trend and benefit from it. Traders should go against human nature.”

– Ramesh Jhunjhunwala

We recently passed the year mark for our Emerging Markets Small Cap portfolio. In a tough environment, there have been markets that have outperformed the EM MSCI Small Cap Index in a substantial way, and we were able to outperform some of those markets. One interesting case has been India, where despite tough valuations, the market has behaved well. MSCI India has outperformed MSCI EM SC by over 23%, according to Bloomberg.

Why does this happen? Why does a market that trades at 20.3 forward price-to-earnings (PE) vs 10.0 MSCI EM SC index (according to Bloomberg, October 5, 2022), massively outperform in this cloudy environment? Referring to the second quote by Ramesh1, when we are investing in India, we are thinking more long term. This is because we are able to find some of the top-quality companies among outstanding trends, which are well managed and are likely to overcome many cycles. India also conveys strong demographic tailwinds and is one of the few EM countries that is actively fostering investing and growth. Will we sometimes have to pay a higher than average index valuations? Probably yes, and that’s fair, because at Global Alpha, we like finding wonderful companies, generating cash flows, low debt and a good balance sheet at a fair price because it’s the core of our process. We are thinking more long term and it is our intention that our bottom-up selection process relates to companies with secular trends that are particularly interesting in the EM space. In the case of India, it is a good match because we can find multiple ideas with secular trends, where EPS growth is followed by stock price appreciation.

India has been our best performing market both year-to-date (YTD), and since inception of the EM Small Cap portfolio. Although we have taken some profits, we continue to like good companies that present interesting investment opportunities. Moreover, the current administration is boosting capex spending, which benefits many sectors. According to Macquarie, the central government spending has increased 34% YTD, driven by spending on roads, railways and defence. Public Sector Undertakings (PSUs) have also increased their spending, and the trend should continue in the remaining part of the year. The private sector is also picking up, albeit not at the same pace, but increasing nonetheless. This has rarely happened in India in the last decade. Public sector spending is concentrated more on infrastructure, while the private sector focuses on renewables, automation and data centres. If we look at this in relative terms, we see some decoupling from India and the rest of the world. Considering the global recession, it’s hard to find countries in the EM space that are fostering investments and growth (Saudi Arabia is another case). As India is a domestic-oriented economy and has an enormous quantity of investment deficits (and opportunities) in different areas, the country can continue with policies that imply growth and investments. While we expect some slowdown in FY24, we anticipate that India should continue with short-mid-term growth that is higher than other countries.

Flow-wise, foreign institutional investors are returning to India. There was a clear sell-off in this market from October 2021, with close to USD 20 billion of outflows, as noted in the CLSA report, Flowmeter: Breakdown of Foreign and domestic flows in India. The market didn’t reflect any major impact basically driven by strong domestic investors’ inflows. In the last three months, we’ve seen foreign direct investment (FDI) coming again to the country, which still conveys strong domestic inflows support. South Africa, Taiwan and Korea have also experienced massive outflows this year. In the two last countries, this is largely explained by its tech-driven markets in a hawkish U.S. Federal Reserve (Fed) environment.

All in all, the equation is not so complicated. Among EM Small Cap, Fed hikes have implied strong outflows in tech-related countries (USD 50 billion between Taiwan and South Korea, according to the CLSA report, Flowmeter: Breakdown of Foreign and domestic flows in India), as China maintains its own internal issues driven by zero Covid policies and the property sector. Some markets, such as Turkey, Chile and Brazil, have outperformed YTD mainly because of low valuations among a hawkish Fed. In the case of India, we think quality structural stories are likely to be favoured in this environment, in domestic oriented market focused economies, with structural demographic tailwinds. We provide two stock examples that have been the key in our outperformance in the Indian market.

Phoenix Mills (PML)

Phoenix Mills is a leading Indian developer of large-format retail-led mixed use developments. Over the last few years, PML has spread its wings across Tier I, II and III cities in India by entering into joint ventures with established regional players and bringing in strategic investors to support the growth of its ongoing and future developments. It differentiates itself by its prime-location assets (currently eight shopping centres) across key cities like Mumbai, Chennai, Bangalore, Pune; steady cash flows; near-term execution visibility; and a healthy balance sheet. PML’s core vision is to create iconic city-centric, mixed-use developments with retail as the core and offices and hotels as complimentary assets, according a HSBC report published June 21, Buy: Growth beyond.

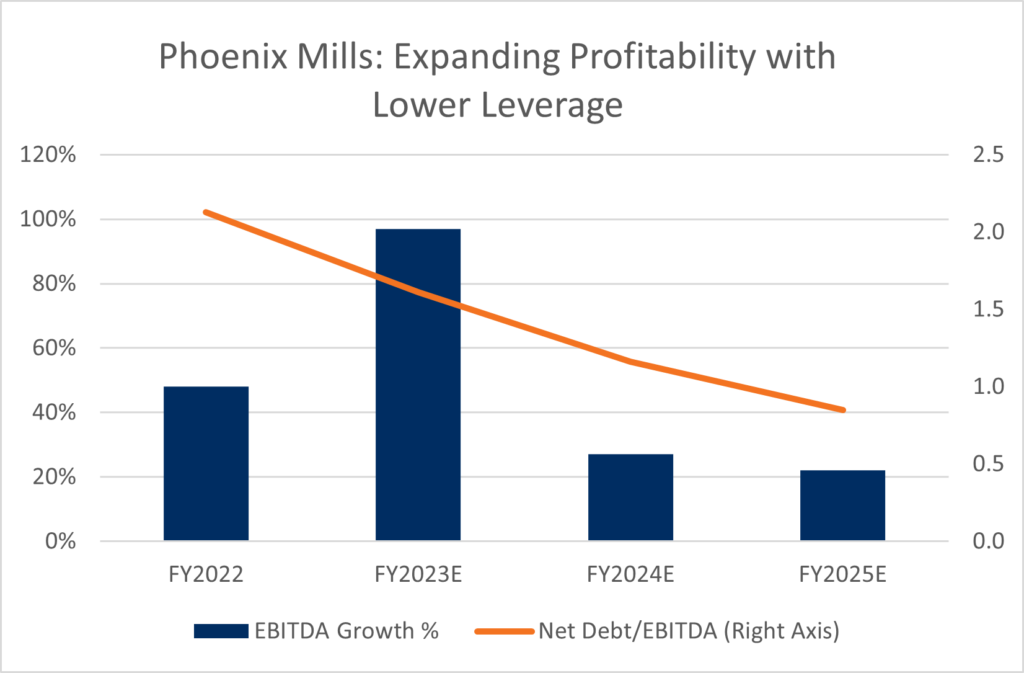

One of PML’s main strengths is the quality of its partners. Phoenix has joint developments with Canadian Pension Plan Investment Board (CPPIB) and Government of Singapore Investment Corporation (GIC). Although both companies have huge investments around the world, it is worth noting that they chose Phoenix Mills as a strategic partner in India. We see the quality and yields of PML projects, a good track record, execution and quality of management as a key differentiator for them in order to establish long-term relationships. Moreover, these partners allow the company to expand their asset base notably with minimum debt requirements. Capex of projects under construction as of Q1FY23 accounted for INR 42 billion and the required corporate debt is only INR 3 billion; that is to say debt funding is at 8% of aggregate capex spends as of Q123, according to a Phoenix Mills presentation from September 2022.

These partnerships are relevant because the company is poised to a strong growth phase, with most of the projects already defined and under construction. From FY22 to FY26, PML plans to increase 1.9 times its gross leasable area (GLA) of shopping centres, from 6.9 millions of square feet (msft) to 13.0 msft (75% consolidated revenues FY24E), and 3.6 times offices GLA, from 2.9 msft to 7.1 msft. Lastly, in its hotels business, the company intends to increase 1.7 times, from 588 keys to 988 keys. To fund this growth, the company has raised equity capital of INR 45 billion, where 75% comes from the capital infusion from its partners.

PML is more than doubling in the next three to four years, with strong global worldwide partners and with almost no additional corporate debt. Currently, at a group level, PML has INR 22 billion of liquidity to fund future growth. The sound financial position of the company has resulted in some local credit rating agencies to upgrade the company. India Ratings and Research upgraded the company to AA- from A+, while maintaining a stable outlook.

In recent months, during an interview, Shishir Shrivastava, Managing Director of Phoenix Mills, expanded more on qualities of the two partners, CPPIB and GIC . He mentioned three pillars worth noting in these comments in a HSBC report published June 21, Buy: Growth beyond:

- “They are long-term investors and bring vast experience and a global relationship, along with

design and costing product specification inputs.” - “They are some of the biggest retail space owners worldwide and have seen how retail has

grown in various countries and thus have a lot to add from that experience.” - “ESG is something Phoenix is learning from their global teams and expanding their

understanding. Overall, they are not silent financial partners.”

In the shopping centre sector, once the group reaches 13.0 million square feet, its GLA should account for roughly 45% of expected GLA of listed companies in India (PML, Prestige, Oberoi, DLF and Brigade). Looking forward, PML has set a target to add approximately 1 million square feet of GLA each year post-FY26 and is looking for greenfield opportunities in various regions, including Kolkata, Surat, Chandigarh, and Hyderabad, among others). Funding would be either solely by PML or with joint venture partner, according to ICICI Securities. Thinking long term, a joint venture with GIC and/or CPPIB can be monetized, for example, by a REIT, or the company can judiciously unlock capital via lease rental discounting (LRD) to continue its expansion, as we see more room for consolidation in the industry.

City Union Bank

City Union Bank Limited is a mid-sized private-sector bank and is also one of the oldest private sector banks in India. The bank is focused on providing working capital finance to small manufacturers and traders with single-banker relationships; 50% of their loan portfolio goes to micro, small and medium enterprises (MSME) and 14% to agriculture.

Driven by its improvement in asset quality and sustained economic recovery, the company revised its FY23 credit growth guidance upwards to 15-18% versus the previous 12-15%. We see this as sustainable with an expected loan book growth of 15-20% and an earnings growth of 20% over the next five years. One of the key competitive advantages for maintaining this is that management is conservative and focused in its core competency of SME lending without falling into the trap of lending to big corporates in risky sectors.

After successfully navigating Covid-led challenges, more significantly within its assessment range, CUBK will be embarking on a higher growth journey hereon. CUBK also enjoys positive tailwinds from increasing capex growth and the financial sector, as explained above. Return on assets should remain at levels of 1.5% (1.46% as of the second quarter), implying return on equity in the range of 15-16%. We think this level of profitability is sustainable for the future, and that’s why valuations are reasonable, both in relation to its history and to other Indian banks. The company has delivered those levels in the past, pre-Covid, which have been stronger than its peers among different business cycles. Net interest margins are steady at 4% and are likely to maintain in that range. Considering the higher proportion of the floating rate book (65% is EBLR linked), asset yields are likely to inch up Q2FY23 onwards. The entire external benchmark based lending rate (EBLR) book is repurchase agreement (repo) linked. With 61% of loan book in working capital loans, repricing is also possible in short intervals.

Several factors give CUBK a key edge over peers and sustain its profitable expansion. The company has a core expertise in high yield SMEs, the company has also been building relationships with the local business community over the years. Additionally, around 99% of the loan book is secured, with high collateral values ensuring that historical loss given default (LGDs) have remained at 30%. CUBK also enjoys a better granular balance sheet on both the asset and liability side than its peers. Dependence on large corporate deposits is low and retail deposits as a percentage of total deposits is 75% (second highest behind the Federal Bank). On the asset side, there is high granularity, with the top 20 borrowers contributing just 5.72% of total assets. Lastly, the total addressable market maintains a big opportunity. Its long runway for growth as MSME’s lending needs are met by private sector banks that now have access to better data with the introduction of GST.

Chart 2: City Union bank current trailing PBV and historical valuation

[1] Ramesh Jhunjhunwala was a very well-known Indian investor who recently passed away. India’s Prime Minister Narendra Modi tweeted after his death: “Full of life, witty and insightful, he lives behind an indelible contribution to the financial world.”