Commentary

Japan’s resurgence

January 25, 2024

Last week, the January edition of the BofA Global Fund Manager Survey was released. It featured 256 panelists who manage a combined US$669 billion in assets. The survey revealed a growing optimism about rate cuts and a macroeconomic “soft landing” despite increasing bearishness with respect to China. Among the many interesting findings, a few are particularly relevant to our focus:

- For the first time since June 2021, there’s a marked preference for small caps over large caps.

- A strong preference for high-quality investments.

- Overweight in countries compared to the average positioning of the past 20 years: notably the US and Japan.

- Overweight in sectors relative to the average positioning in the past two decades: predominantly in consumer staples, healthcare and technology.

While our last commentary covered global small caps in general, this week let’s take a closer look at Japan specifically. The positive sentiment towards Japan in the survey is in line with market trends. The Nikkei 225 Index was up 28% in 2023 and recently reached its highest level in 34 years, approaching a new record.

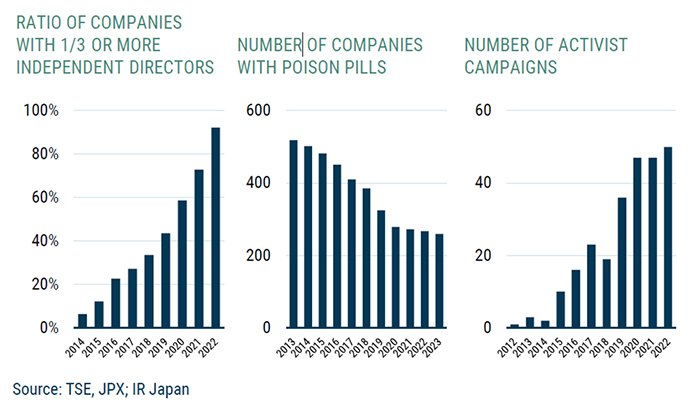

Factors driving this rally include a weaker yen, the end of deflation, wage growth and improved corporate governance. A decade ago, few companies had independent directors, but today almost all have at least a third of their board as independents. Institutional investors are increasingly voting down poison pills and supporting activism.

Source: GMO.

In 2024, we expect continuing financial reforms to attract more investors. Here are some new initiatives:

- January: Introduction of the revamped Nippon Individual Savings Account (NISA). Under Prime Minister Kishida’s new capitalism scheme, the NISA aims to boost household wealth through investment. The contribution limit has been raised and the tax-exempt period extended, allowing an annual contribution of up to ¥3.6 million (US$24,300) per person and a combined total balance of ¥18 million to be permanently tax exempt. As of June 2023, there were 19.4 million NISA accounts, a modest number considering Japan’s population. In contrast, Japanese households held a record ¥2,115 trillion in financial assets, with more than half of this amount in cash.

- January 15: Companies on the Tokyo Stock Exchange (TSE) began disclosing their capital efficiency plans. Thus far, 40% of firms listed in the TSE’s prime section have done so.

- April: Enhanced segment earnings reporting. In addition to quarterly earnings reports, listed companies will now only need to submit more detailed financial reports semiannually rather than quarterly. This change emphasizes segment reporting. The TSE will mandate that companies disclose earnings and cashflow for each business segment to improve transparency.

- November 5: The TSE will extend trading hours by 30 minutes to increase liquidity.

How have Japanese small caps been performing?

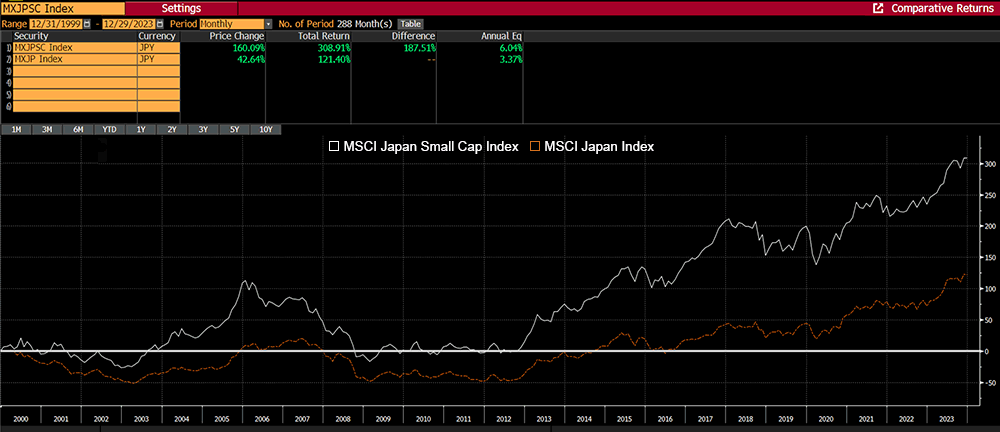

Since 2000, Japanese small caps have substantially outperformed large caps.

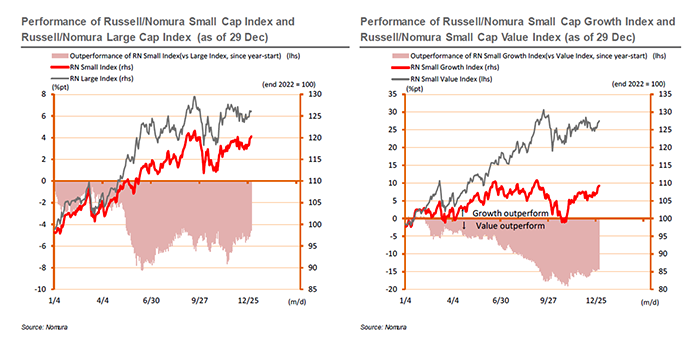

However, in 2023, they underperformed, with value stocks outperforming growth stocks. This trend was influenced by the TSE’s March 2023 initiative for sustainable growth and enhanced corporate value, leading to a renewed interest in large caps and companies with a price/book value below 1x.

Looking ahead, we believe strong fundamentals and valuations are likely to favour Japanese small caps over large caps due to:

- Faster earnings growth: Bloomberg data predicts +20% EPS growth for the MSCI Japan Small Cap Index in the next 12 months compared to +8% for the MSCI Japan Index. EPS growth for the following 12 months is +12% for the MSCI Japan Small Cap Index and +10% for the MSCI Japan Index.

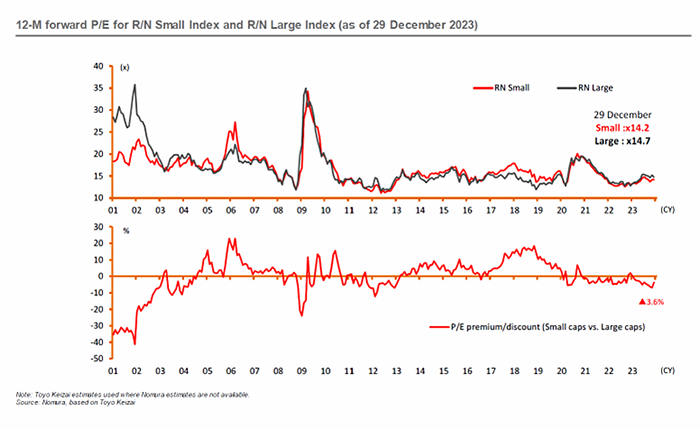

- Cheaper valuations: The P/E multiple discount for Japanese small caps compared to large caps widened in 2023 to a sizable 3.6%, suggesting a potential mean reversion.

- Reduced FX volatility: We expect the JPY to appreciate against the USD in 2024 in response to monetary policy in the US and Japan. Japanese small caps, which are more exposed to the stable domestic economy than large caps, should be less affected by currency fluctuations and may even benefit from a stronger yen via imports.

We believe the shift towards Japanese markets and small-cap stocks hints at something deeper than market fluctuations and could be indicative of structural changes and a broader reassessment of risk and opportunity. Moving forward, investors may need to view traditional powerhouses through a new lens and consider how different markets and different asset classes can offer new avenues for growth in a world where economic certainties are increasingly hard to come by.