Commentary

Entrepreneurship: Silicon Valley vs. Stockholm

January 23, 2025

Amid the overall pessimism toward European economies, one of the reasons provided most often for the underperformance relative to the United States is a lack of innovation and entrepreneurship. Many data points tend to confirm this:

- Over three times as many patents are filed in the United States annually than the entirety of Europe.

- Research and development (R&D) is 2.8% of GDP in the United States vs. only 2.2% for Europe.

- Average time to go through filings to start a business is 3-5 days in the United States and up to multiple weeks in Europe.

- The United States attracts the lion’s share of global venture capital (VC) investment; over three times of the $50 billion attracted by Europe in 2023.

It is worth noting, however, that Europe has one large outlier when it comes to innovation: Sweden. Within Europe, Sweden easily stands out as one of the most entrepreneurial and innovative countries, raising questions from its neighbours as to how their success can be replicated. While entrepreneurship metrics have, by some measures, declined in the United States over the past 30 years, Sweden has seen the opposite trend.

So, what differentiates Sweden from its neighbours, and can it be replicated?

There is a case to be made that part of it stems from a cultural aspect. Swedish demographics have historically been described as high on social trust and cohesiveness, driven by a small historical level of immigration, similar to Japan or South Korea, but it is probably only part of the overall picture. Other likely factors include:

- Entrepreneurship training in Sweden being taught in high school since 1980, with over 30% of students today participating in such programs. Other Nordic countries, on the other hand, started this type of program only in the mid-1990s and on a much smaller scale than Sweden did.

- Risk-taking being socially encouraged and celebrated, with a common perception that opportunities are plentiful. Social safety nets also allow for failure and risk-taking.

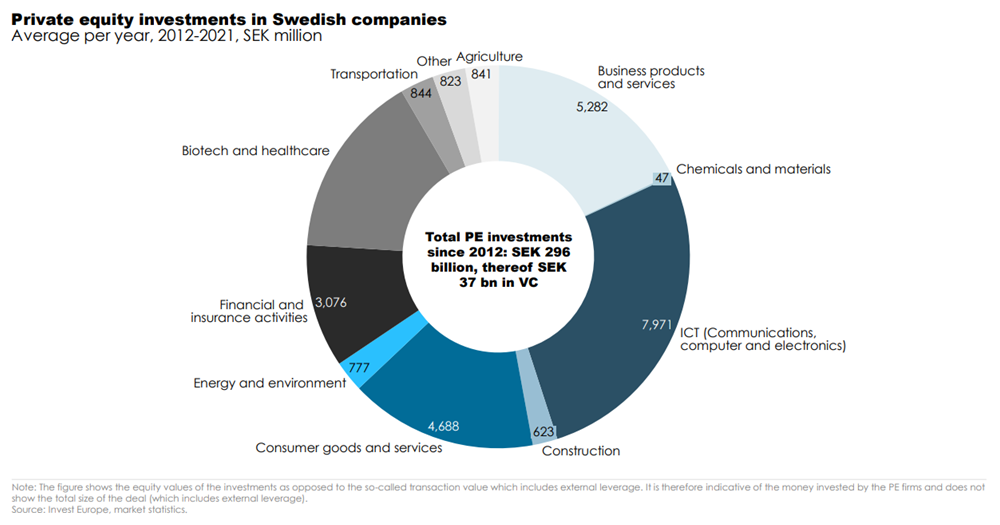

Possibly as a result of this, Sweden’s VC market is more vibrant than other Nordic countries and has contributed directly to building Sweden’s reputation as a hub for technological innovation through its higher focus on early-stage investments. Furthermore, VC investment is well supported by the government through tax-incentives, grants and funding programs. Consequently, Sweden has the largest private equity capital raised as a share of GDP in Europe, trailing only Luxembourg. On its own, Swedish VC is estimated to have contributed 1.5% of total GDP growth on its own and has had a direct impact on creating more highly skilled, specialized jobs than its neighbouring countries.

It is therefore no surprise that Global Alpha is quite positive on Sweden’s long-term prospects and has had no trouble finding quality names for our portfolios. We profile two such names here.

Sdiptech AB (SDIPB SS) is a so-called industrial “serial acquirer,” a unique Sweden-based business model that consists of growth mostly through small, niche acquisitions without necessarily seeking material synergies or trying to integrate with the existing businesses. It acts as a forever-owner of companies where the founder is looking to sell their business, make sure their employees are well taken care of and don’t want to sell to private equity. Sdiptech focuses on acquiring businesses that are already cash-flow generative, as it finances its acquisitions purely through debt and not equity dilution. Its acquired companies operate along one of the four segments of its reporting structure: supply chain & transportation, water & bioeconomy, safety & security and energy & electrification. Most of its sales are aligned with the UN societal development goals. The company also differentiates itself from other serial acquirers through its comparatively strong organic growth profile (in addition to consistent M&As) and its lower leverage than peers, resulting from its smaller scale and more focused end-markets.

Another company we own in Sweden is Biogaia AB (BIOGB SS), a producer of probiotic supplements founded in 1990 by Peter Rothschild and that is present in over 100 markets. Probiotics is a USD71 billion global market with an expected CAGR of 8% over the next five years, driven by higher health awareness and shifting preference toward preventive healthcare. Biogaia differentiates itself from peers on two aspects: its global reach and its science-driven, innovative approach to product development. Biogaia is the only probiotic provider that continuously collaborates with universities globally on research to maintain its differentiated product from more generic peers who usually spend less than 1% of their sales on R&D, allowing it to sell at a premium with less discounting than its competitors.

It is probably an overstatement to say that Sweden is better today at fostering innovation than its North American counterpart. Nonetheless, it is noteworthy that Sweden has been trending more toward a dynamic bottom-up approach to innovating whereas observers tend to agree that the US economy has evolved into an environment that tends to favour incumbents over new entrants, thanks to softer regulations around lobbying and a higher rate of regulatory capture. We remain globally diversified and are optimistic on the growth prospects of both the United States and Sweden going into this new year.